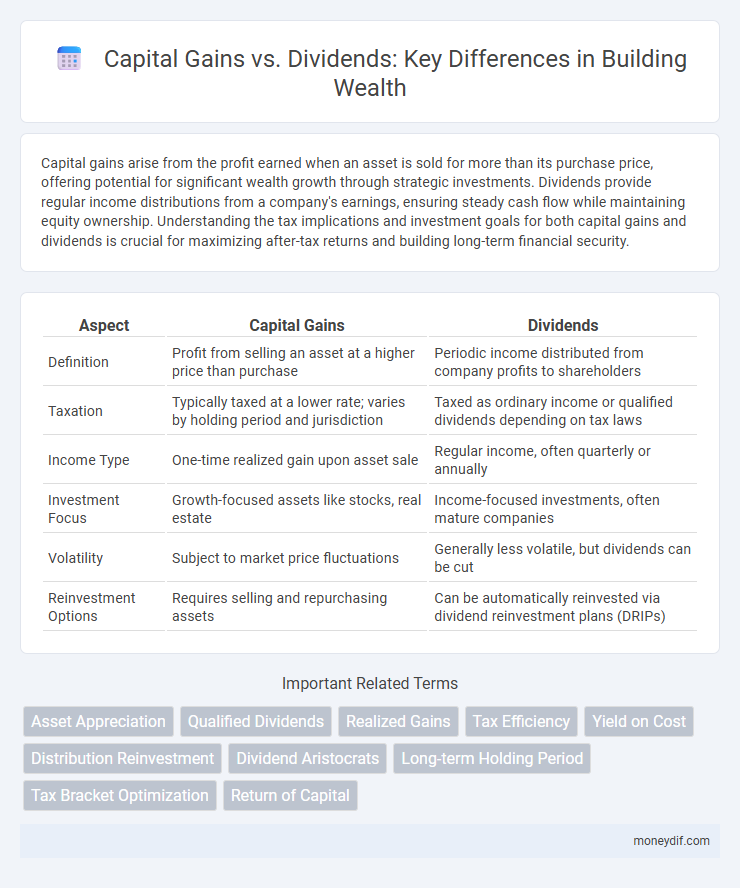

Capital gains arise from the profit earned when an asset is sold for more than its purchase price, offering potential for significant wealth growth through strategic investments. Dividends provide regular income distributions from a company's earnings, ensuring steady cash flow while maintaining equity ownership. Understanding the tax implications and investment goals for both capital gains and dividends is crucial for maximizing after-tax returns and building long-term financial security.

Table of Comparison

| Aspect | Capital Gains | Dividends |

|---|---|---|

| Definition | Profit from selling an asset at a higher price than purchase | Periodic income distributed from company profits to shareholders |

| Taxation | Typically taxed at a lower rate; varies by holding period and jurisdiction | Taxed as ordinary income or qualified dividends depending on tax laws |

| Income Type | One-time realized gain upon asset sale | Regular income, often quarterly or annually |

| Investment Focus | Growth-focused assets like stocks, real estate | Income-focused investments, often mature companies |

| Volatility | Subject to market price fluctuations | Generally less volatile, but dividends can be cut |

| Reinvestment Options | Requires selling and repurchasing assets | Can be automatically reinvested via dividend reinvestment plans (DRIPs) |

Understanding Capital Gains and Dividends

Capital gains arise from the profit earned when an asset is sold for more than its purchase price, often subject to favorable tax rates if held long-term. Dividends represent periodic payments distributed by corporations to shareholders, reflecting a share of the company's earnings. Recognizing the difference between capital gains and dividends is essential for optimizing investment strategies and tax planning within wealth management.

Key Differences Between Capital Gains and Dividends

Capital gains arise from the profit earned when an asset is sold for more than its purchase price, while dividends represent regular income distributed from a company's earnings to shareholders. Capital gains are typically taxed based on holding periods, with long-term gains often receiving favorable rates, whereas dividends may be taxed as ordinary income or qualified dividends with preferential rates. Investors often prioritize capital gains for growth and dividends for steady income, reflecting different strategies in wealth accumulation and portfolio management.

How Capital Gains Work in Wealth Building

Capital gains represent the profit earned from the sale of assets such as stocks, real estate, or mutual funds, playing a crucial role in wealth building by allowing investors to grow their capital over time. Unlike dividends, which provide regular income, capital gains accumulate and compound, benefiting from long-term investment strategies and tax-advantaged accounts like IRAs or 401(k)s. Maximizing capital gains involves strategic asset allocation, timing market conditions, and reinvesting profits to enhance overall portfolio growth.

The Role of Dividends in Passive Income

Dividends play a crucial role in passive income by providing a steady and predictable cash flow from investments without the need to sell assets. Unlike capital gains, which rely on market timing and asset appreciation for profit realization, dividends offer consistent income streams that can be reinvested or used for expenses. High-dividend-yield stocks and dividend growth investing strategies enhance portfolio stability and long-term wealth accumulation through compounding returns.

Tax Implications: Capital Gains vs. Dividends

Capital gains are generally taxed at a lower rate than ordinary income, benefiting investors who hold assets for more than a year due to preferential long-term capital gains tax rates. Dividends, especially qualified dividends, are also taxed at favorable rates but can be taxed as ordinary income if they are non-qualified. Understanding the different tax treatments of capital gains and dividends is crucial for optimizing after-tax returns in wealth management.

Strategies to Maximize Capital Gains

Maximizing capital gains involves strategically timing asset sales to benefit from long-term capital gains tax rates, which are typically lower than ordinary income tax rates on dividends. Diversifying portfolios with growth-oriented stocks and reinvesting gains through tax-advantaged accounts, such as IRAs or 401(k)s, can enhance wealth accumulation. Employing tax-loss harvesting to offset realized gains further optimizes after-tax returns.

Dividend Investing: Pros and Cons

Dividend investing offers consistent income streams through regular payouts from profitable companies, making it attractive for investors seeking steady cash flow. However, dividends are subject to taxation, which can reduce overall returns compared to capital gains that benefit from lower tax rates when assets appreciate and are sold. The main drawback lies in dividend cuts during economic downturns, impacting income reliability, while capital gains provide growth potential without income fluctuations.

Risk Factors: Capital Gains vs. Dividend Income

Capital gains expose investors to market volatility and potential loss as asset prices fluctuate, while dividend income generally provides a steadier cash flow with lower risk due to periodic payments from established companies. However, dividend payments can be cut or suspended during economic downturns, impacting income stability. Assessing the risk factors involves considering market conditions, company performance, and individual financial goals to balance growth potential against income reliability.

Which is Better for Long-Term Wealth?

Capital gains often provide greater wealth accumulation over the long term due to their potential for compound growth and favorable tax treatment, especially when assets are held for more than a year. Dividends offer steady income streams and may appeal to investors seeking regular cash flow, but they are typically taxed as ordinary income, which can reduce net returns. Understanding the investor's time horizon, tax bracket, and financial goals is critical in determining whether capital gains or dividends better support long-term wealth building.

Choosing the Right Approach for Your Financial Goals

Capital gains offer potential for higher long-term growth through asset appreciation, while dividends provide steady income streams ideal for risk-averse investors seeking cash flow. Evaluating tax implications and investment horizon helps determine whether a focus on capital gains or dividend income aligns best with your overall financial objectives. Balancing both strategies can optimize portfolio diversification and wealth accumulation based on individual risk tolerance and liquidity needs.

Important Terms

Asset Appreciation

Asset appreciation refers to the increase in the value of an investment over time, which contributes to capital gains when the asset is sold at a higher price than its purchase cost. Unlike dividends, which provide regular income distributions, capital gains result from the growth in asset value and are subject to different tax treatment depending on the holding period and jurisdiction.

Qualified Dividends

Qualified dividends receive favorable tax treatment by being taxed at the lower long-term capital gains rates, which range from 0% to 20% depending on income level, contrasting with ordinary dividends taxed at higher ordinary income rates. Investors benefit tax-efficient income streams through qualified dividends, positioning them advantageously compared to non-qualified dividends that do not qualify for capital gains rates and face higher tax liabilities.

Realized Gains

Realized gains refer to the actual profit earned from selling an asset, such as stocks or real estate, and are subject to capital gains tax rates, which typically differ from tax rates applied to dividends. Capital gains are categorized as short-term or long-term based on asset holding periods, while dividends represent income distributions from investments and are taxed at qualified or ordinary income rates.

Tax Efficiency

Capital gains often benefit from lower tax rates compared to dividends, especially qualified dividends which may be taxed similarly but depend on holding periods and income brackets. Strategic portfolio management focusing on long-term capital gains can enhance tax efficiency by minimizing tax liabilities and maximizing after-tax returns.

Yield on Cost

Yield on Cost measures the annual dividend income relative to the original investment price, highlighting income growth through capital gains reinvested into dividends. This metric helps investors compare the effectiveness of dividend payments against potential capital gains for overall portfolio returns.

Distribution Reinvestment

Distribution reinvestment allows investors to automatically use dividends and capital gains distributions to purchase additional shares, enhancing compounding effects. Unlike dividends taxed as ordinary income, capital gains distributions often benefit from lower tax rates, making reinvestment strategies crucial for tax-efficient portfolio growth.

Dividend Aristocrats

Dividend Aristocrats are S&P 500 companies that have increased dividends for at least 25 consecutive years, offering a stable source of income compared to capital gains, which depend on stock price appreciation and can be more volatile. Investors often prefer Dividend Aristocrats for consistent dividend income, which may be taxed differently than capital gains, potentially impacting after-tax returns.

Long-term Holding Period

Long-term holding period reduces capital gains tax rates compared to short-term holdings, often resulting in preferential rates of 0%, 15%, or 20% depending on income brackets. Dividends, categorized as qualified or non-qualified, are taxed differently--qualified dividends benefit from the same reduced rates as long-term capital gains, while non-qualified dividends are taxed at ordinary income tax rates.

Tax Bracket Optimization

Tax bracket optimization strategically manages investments to minimize tax liabilities by aligning capital gains and dividends with the investor's tax bracket. Long-term capital gains and qualified dividends often benefit from lower tax rates compared to ordinary income, making timing and income allocation crucial for maximizing after-tax returns.

Return of Capital

Return of Capital reduces the original investment basis, decreasing the immediate taxable income compared to dividends, which are typically taxed as ordinary income or qualified dividends. Capital gains arise when the investment is sold for more than the adjusted basis, making Return of Capital an effective strategy to defer taxes until the sale event.

Capital Gains vs Dividends Infographic