SWIFT and CHIPS are essential payment networks used in international and domestic banking transactions. SWIFT provides a global messaging system that enables secure communication of payment instructions across banks worldwide, while CHIPS primarily handles high-value USD payments within the United States. The choice between SWIFT and CHIPS depends on transaction scope, speed requirements, and regional preferences in cross-border and domestic fund transfers.

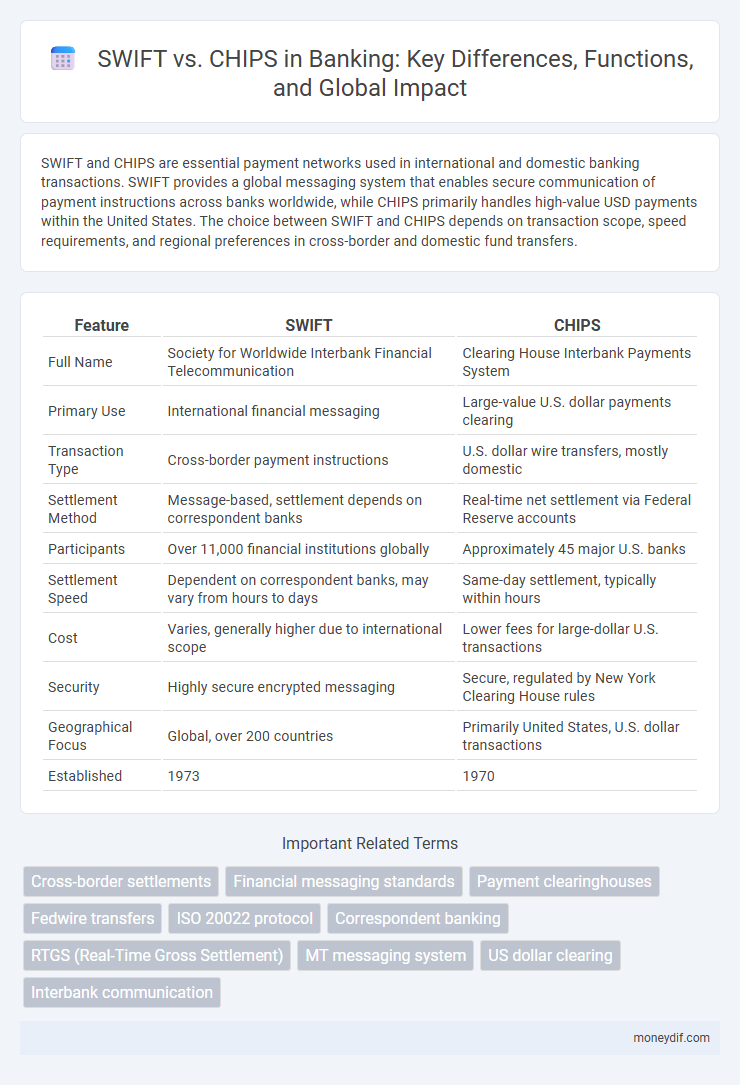

Table of Comparison

| Feature | SWIFT | CHIPS |

|---|---|---|

| Full Name | Society for Worldwide Interbank Financial Telecommunication | Clearing House Interbank Payments System |

| Primary Use | International financial messaging | Large-value U.S. dollar payments clearing |

| Transaction Type | Cross-border payment instructions | U.S. dollar wire transfers, mostly domestic |

| Settlement Method | Message-based, settlement depends on correspondent banks | Real-time net settlement via Federal Reserve accounts |

| Participants | Over 11,000 financial institutions globally | Approximately 45 major U.S. banks |

| Settlement Speed | Dependent on correspondent banks, may vary from hours to days | Same-day settlement, typically within hours |

| Cost | Varies, generally higher due to international scope | Lower fees for large-dollar U.S. transactions |

| Security | Highly secure encrypted messaging | Secure, regulated by New York Clearing House rules |

| Geographical Focus | Global, over 200 countries | Primarily United States, U.S. dollar transactions |

| Established | 1973 | 1970 |

Overview of SWIFT and CHIPS

SWIFT (Society for Worldwide Interbank Financial Telecommunication) provides a global messaging network facilitating secure and standardized communication for international financial transactions among over 11,000 banking institutions in more than 200 countries. CHIPS (Clearing House Interbank Payments System) is a US-based electronic payment system managing large-value domestic and international dollar transactions, processing around $1.7 trillion daily through its netting capabilities to reduce settlement risk. Both systems are integral to global banking infrastructure, with SWIFT focusing on message exchange and CHIPS on efficient payment clearing and settlement.

Key Functions of SWIFT in Global Banking

SWIFT facilitates secure and standardized financial messaging for over 11,000 banks and institutions worldwide, enabling seamless cross-border payments and trade finance. It provides a unified communication platform that supports payment instructions, foreign exchange confirmations, and securities transactions. SWIFT's network ensures transparency, compliance with international regulations, and real-time transaction tracking, which is critical for global banking operations.

Core Features of CHIPS Payment Network

CHIPS (Clearing House Interbank Payments System) is a large-value payment system specializing in U.S. dollar transactions, providing real-time finality and net settlement among member banks. Unlike SWIFT, which is primarily a messaging network for cross-border payments, CHIPS facilitates the clearing and settlement of domestic and international dollar payments within a single integrated platform. Its core features include bilateral netting, high transaction capacity, multilaterally optimized netting, and 24-hour availability to support large financial institutions and multinational corporations.

SWIFT vs CHIPS: Transaction Speed Comparison

SWIFT processes international transactions typically within 24 to 48 hours, as it relies on correspondent banking networks and manual verification steps; in contrast, CHIPS settles large-value USD payments in real-time, often within minutes, using a netting system that optimizes liquidity. SWIFT's global messaging infrastructure supports over 11,000 financial institutions in 200+ countries, prioritizing universality over speed. CHIPS, managed by The Clearing House, specializes in domestic and international USD transactions, offering faster settlement crucial for time-sensitive corporate and interbank transfers.

Security Protocols in SWIFT and CHIPS

SWIFT employs robust security protocols including strong encryption, multi-factor authentication, and continuous monitoring to safeguard financial messages across its global network. CHIPS utilizes advanced encryption standards and stringent access controls tailored for high-value dollar payments, ensuring transactional integrity and confidentiality within the US domestic banking system. Both networks prioritize secure message transmission but differ in protocol specifics due to their distinct operational scopes and regulatory environments.

Geographic Reach and Network Coverage

SWIFT enables global financial messaging with over 11,000 institutions across 200 countries, providing extensive geographic reach for international banking transactions. CHIPS operates primarily within the United States, connecting major U.S. and international banks but with limited geographic coverage compared to SWIFT. While SWIFT supports a broad network for cross-border payments, CHIPS specializes in high-value dollar transactions within a concentrated U.S. network.

Cost Implications: SWIFT vs CHIPS

SWIFT transactions typically incur higher fees due to intermediary banks and global network charges, while CHIPS offers cost advantages for high-value US dollar payments through a single clearinghouse with lower transaction fees. Banks using CHIPS benefit from reduced operational costs and faster settlement times, enhancing liquidity management. The choice between SWIFT and CHIPS significantly impacts overall transaction expenses, especially for cross-border versus domestic payments.

Compliance and Regulatory Considerations

SWIFT and CHIPS operate under distinct compliance and regulatory frameworks, with SWIFT adhering to international standards like AML and KYC protocols across 200+ countries, facilitating global financial communication while ensuring regulatory oversight. CHIPS, primarily focused on U.S. dollar transactions within the United States, complies with U.S. regulations enforced by the Federal Reserve, emphasizing strict adherence to OFAC sanctions and FinCEN guidelines. Financial institutions using SWIFT must navigate diverse jurisdictional requirements, whereas CHIPS participants benefit from centralized regulatory scrutiny, impacting risk management and reporting obligations.

Use Cases: When to Choose SWIFT or CHIPS

SWIFT excels in global cross-border payments, facilitating secure communication between over 11,000 financial institutions in more than 200 countries, ideal for international trade finance and correspondent banking. CHIPS is preferred for high-value, USD-denominated domestic and cross-border transactions within the United States, offering real-time settlement and reducing counterparty risk for large corporate and interbank transfers. Financial institutions choose SWIFT for its extensive global network and standardized messaging, while CHIPS is selected for speed and efficiency in U.S. dollar clearing.

Future Trends in Cross-Border Payments Systems

SWIFT is evolving with enhanced real-time messaging capabilities and integration of blockchain technology to improve transparency and reduce settlement times. CHIPS focuses on increasing interoperability with emerging digital currency platforms and expanding its network to support higher transaction volumes securely. Both systems are driving innovation to meet the growing demand for faster, more efficient, and cost-effective cross-border payments.

Important Terms

Cross-border settlements

Cross-border settlements rely heavily on SWIFT for secure, standardized financial messaging across global banks, facilitating efficient communication and transaction processing. CHIPS handles large-value USD payments domestically in the U.S. with real-time settlement finality, making it faster for high-value trades but limited in international messaging capabilities.

Financial messaging standards

SWIFT (Society for Worldwide Interbank Financial Telecommunication) provides a global messaging network facilitating international bank transactions using standardized formats like MT and ISO 20022, ensuring interoperability among over 11,000 financial institutions. CHIPS (Clearing House Interbank Payments System) operates as a U.S.-based large-value payment system primarily for domestic dollar transactions, employing proprietary message formats optimized for high-value, time-sensitive fund transfers within the U.S. banking network.

Payment clearinghouses

SWIFT (Society for Worldwide Interbank Financial Telecommunication) facilitates secure global financial messaging, enabling banks to exchange payment instructions internationally, while CHIPS (Clearing House Interbank Payments System) is a U.S.-based large-value payment system that processes high-value, time-sensitive USD transactions primarily for domestic and cross-border settlements. SWIFT operates as a messaging network without settling funds, whereas CHIPS functions as a clearinghouse that nets payments and provides final settlement, reducing liquidity needs for participating banks.

Fedwire transfers

Fedwire transfers leverage the Federal Reserve's real-time gross settlement system to process large-value transactions domestically in the United States, offering immediate finality and settlement. In contrast, SWIFT serves as a global messaging network facilitating international payment instructions, while CHIPS operates as a U.S.-based private clearing system specializing in high-value dollar payments, often providing net settlement to optimize liquidity.

ISO 20022 protocol

ISO 20022 is a global messaging standard designed to enhance interoperability and efficiency in financial communications, increasingly adopted by SWIFT for cross-border payments to provide richer, structured data. CHIPS, primarily a U.S.-based large-value payment system, is also aligning with ISO 20022 to improve transaction transparency and streamline clearing processes, fostering greater compatibility with international networks like SWIFT.

Correspondent banking

Correspondent banking relies heavily on messaging networks like SWIFT and CHIPS to facilitate cross-border transactions, with SWIFT offering a global communication platform for secure payment instructions and CHIPS providing a high-value domestic payment system in the United States. SWIFT supports over 11,000 financial institutions worldwide, enabling international correspondent banking relationships, while CHIPS handles approximately $1.7 trillion in daily U.S. dollar transactions, optimizing liquidity management and settlement speed.

RTGS (Real-Time Gross Settlement)

RTGS (Real-Time Gross Settlement) systems enable immediate fund transfers between banks, with SWIFT providing the secure messaging network for international RTGS transactions, while CHIPS operates as a U.S.-based large-value payment system that settles net positions in real time. SWIFT facilitates global interoperability for RTGS by connecting financial institutions worldwide, whereas CHIPS focuses on clearing and settling high-value USD payments within the U.S. banking system.

MT messaging system

MT messaging system facilitates standardized financial messages within the SWIFT network, ensuring secure and efficient cross-border transactions. CHIPS operates as a large-value payment system mainly in the U.S., utilizing proprietary messages for high-value domestic payments unlike the globally recognized SWIFT MT format.

US dollar clearing

US dollar clearing involves the settlement of dollar-denominated transactions through international banking networks, primarily facilitated by SWIFT and CHIPS systems. Unlike SWIFT, which provides a global messaging platform for secure financial communication, CHIPS operates as a U.S.-based large-value payment system specializing in net settlement of high-value dollar transactions, thereby enhancing liquidity efficiency and reducing cross-border payment risks.

Interbank communication

SWIFT facilitates secure, standardized messaging for international interbank communication, enabling cross-border payments in over 200 countries with extensive network connectivity. CHIPS operates as a U.S.-based large-value payment system optimizing high-value, dollar-denominated transactions with real-time net settlement, primarily serving domestic financial institutions.

SWIFT vs CHIPS Infographic