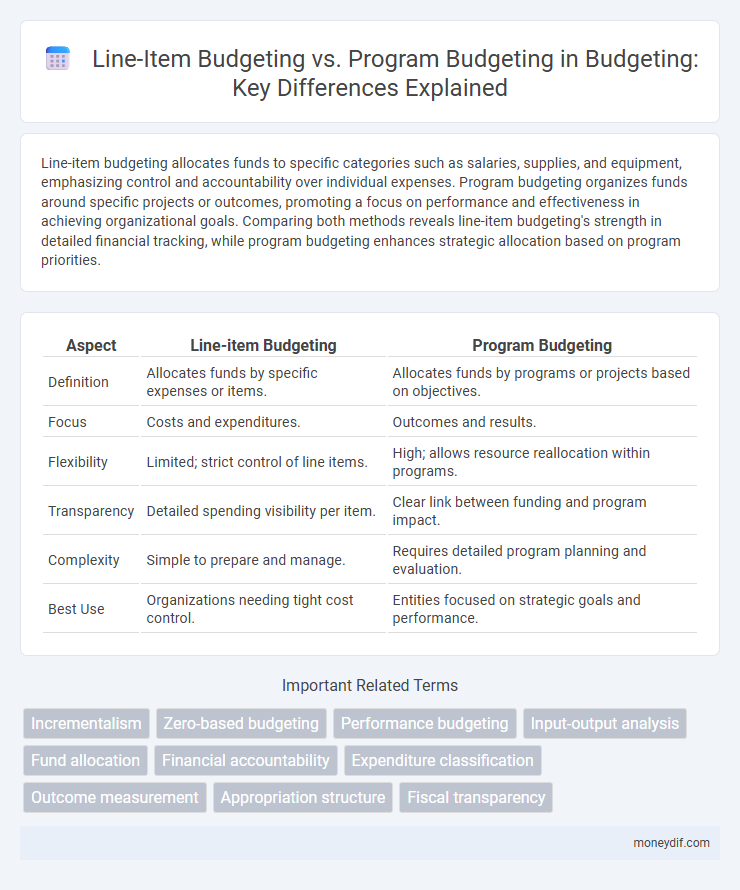

Line-item budgeting allocates funds to specific categories such as salaries, supplies, and equipment, emphasizing control and accountability over individual expenses. Program budgeting organizes funds around specific projects or outcomes, promoting a focus on performance and effectiveness in achieving organizational goals. Comparing both methods reveals line-item budgeting's strength in detailed financial tracking, while program budgeting enhances strategic allocation based on program priorities.

Table of Comparison

| Aspect | Line-item Budgeting | Program Budgeting |

|---|---|---|

| Definition | Allocates funds by specific expenses or items. | Allocates funds by programs or projects based on objectives. |

| Focus | Costs and expenditures. | Outcomes and results. |

| Flexibility | Limited; strict control of line items. | High; allows resource reallocation within programs. |

| Transparency | Detailed spending visibility per item. | Clear link between funding and program impact. |

| Complexity | Simple to prepare and manage. | Requires detailed program planning and evaluation. |

| Best Use | Organizations needing tight cost control. | Entities focused on strategic goals and performance. |

Introduction to Budgeting Approaches

Line-item budgeting allocates funds to specific expense categories, providing detailed tracking of expenditures, while program budgeting focuses on funding based on specific objectives and outcomes to improve resource allocation efficiency. Line-item budgeting emphasizes control and accountability over costs, whereas program budgeting aligns spending with strategic goals to enhance decision-making and performance evaluation. Understanding these approaches helps organizations choose budgeting methods that best support financial planning and operational priorities.

What is Line-Item Budgeting?

Line-item budgeting allocates funds by specific categories such as salaries, supplies, and equipment, providing clear and detailed expense tracking for each budget line. This traditional budget method emphasizes control and accountability by defining exact amounts for each expenditure item, making it easier to monitor variances and compliance. Line-item budgeting is widely used in both public and private sectors for straightforward financial management and reporting.

What is Program Budgeting?

Program budgeting allocates financial resources based on specific programs or goals, emphasizing outcomes and performance rather than individual expense categories. This method enhances transparency and accountability by linking budget expenditures to measurable results and objectives. By prioritizing strategic initiatives, program budgeting facilitates more effective resource management and better alignment with organizational priorities.

Key Components of Line-Item Budgeting

Line-item budgeting primarily focuses on categorizing expenses into specific, detailed accounts such as salaries, office supplies, and utilities, allowing precise tracking and control over individual cost elements. This budgeting method emphasizes clear allocation of funds to distinct budget items, facilitating straightforward comparison between projected and actual expenditures. Key components include expenditure categories, allocated amounts, and clear documentation of each line item's purpose and justification.

Core Elements of Program Budgeting

Program budgeting centers on aligning financial resources with specific organizational goals, incorporating core elements such as defining clear program objectives, identifying relevant activities, and estimating associated costs. Unlike line-item budgeting, which itemizes expenses by category, program budgeting emphasizes outcomes by grouping expenditures under thematic programs to enhance accountability and effectiveness. This approach facilitates strategic planning by linking budget allocation directly to measurable results and performance indicators.

Comparative Analysis: Line-Item vs Program Budgeting

Line-item budgeting allocates funds by specific categories such as salaries, equipment, and supplies, providing detailed control and straightforward tracking but often limiting flexibility in resource allocation. Program budgeting organizes funds based on distinct projects or programs, enhancing goal orientation and performance evaluation while requiring comprehensive planning and coordination. Comparing both, line-item budgeting excels in fiscal discipline, whereas program budgeting better supports strategic decision-making aligned with organizational objectives.

Advantages of Line-Item Budgeting

Line-item budgeting offers clear advantages by providing detailed transparency and control over individual expense categories, making it easier to track spending and ensure accountability. This method simplifies financial management through straightforward categorization of costs, which facilitates easy comparison and auditing. Its structured format helps organizations identify cost-saving opportunities by highlighting specific budget items.

Benefits of Program Budgeting

Program budgeting enhances transparency by clearly linking funds to specific outcomes and objectives, improving accountability in public financial management. It facilitates strategic resource allocation that aligns with organizational goals, optimizing the impact of expenditures. This approach also supports better performance evaluation by enabling detailed tracking of program effectiveness and cost-efficiency.

Challenges and Limitations of Each Method

Line-item budgeting faces challenges such as limited flexibility and difficulty in linking expenditures to outcomes, which restricts its effectiveness in performance evaluation. Program budgeting, while offering a results-oriented approach, encounters limitations including complexity in implementation, high data requirements, and potential misalignment between programs and actual organizational goals. Both methods require robust management systems to address their inherent limitations and optimize resource allocation efficiency.

Choosing the Right Budgeting Approach for Your Organization

Line-item budgeting offers detailed control over expenses by categorizing costs into specific accounts, ideal for organizations requiring strict financial oversight and regulatory compliance. Program budgeting aligns resources with organizational goals by focusing on funding specific projects or outcomes, enhancing strategic planning and performance evaluation. Choosing the right budgeting approach depends on organizational priorities, complexity, and desire for transparency versus flexibility in resource allocation.

Important Terms

Incrementalism

Incrementalism in budgeting emphasizes small, gradual changes to line-item budgets, contrasting with program budgeting's focus on outcome-based allocations and strategic resource reallocation.

Zero-based budgeting

Zero-based budgeting allocates funds based on detailed justification from zero, contrasting line-item budgeting which focuses on specific expenses and program budgeting which emphasizes funding linked to organizational goals and outcomes.

Performance budgeting

Performance budgeting links allocated funds to measurable outcomes, contrasting with line-item budgeting's focus on expenses by category and program budgeting's emphasis on funding specific initiatives.

Input-output analysis

Input-output analysis quantifies resource flows and outputs, providing detailed data that enhances accuracy in line-item budgeting, while program budgeting focuses on broader goals and outcomes, emphasizing cost-effectiveness rather than granular input-output measurement.

Fund allocation

Fund allocation through line-item budgeting focuses on specific expense categories for granular control, while program budgeting prioritizes funding based on program objectives and outcomes to enhance strategic resource distribution.

Financial accountability

Financial accountability improves as line-item budgeting provides detailed expense tracking while program budgeting aligns expenditures with organizational goals for better resource allocation.

Expenditure classification

Line-item budgeting allocates funds based on specific expense categories, whereas program budgeting classifies expenditures according to objectives and outcomes of distinct programs.

Outcome measurement

Outcome measurement evaluates program budgeting effectiveness by linking financial inputs directly to results, unlike line-item budgeting which focuses solely on tracking expenditures without assessing impact.

Appropriation structure

Appropriation structure in line-item budgeting emphasizes detailed expenditure categories, whereas program budgeting allocates funds based on specific programs and their objectives for enhanced outcome alignment.

Fiscal transparency

Fiscal transparency improves when line-item budgeting clearly itemizes government expenditures by categories such as salaries and supplies, facilitating straightforward tracking of spending. Program budgeting enhances fiscal transparency by linking expenditures to specific government objectives and outcomes, enabling more effective evaluation of resource allocation and program performance.

Line-item budgeting vs Program budgeting Infographic