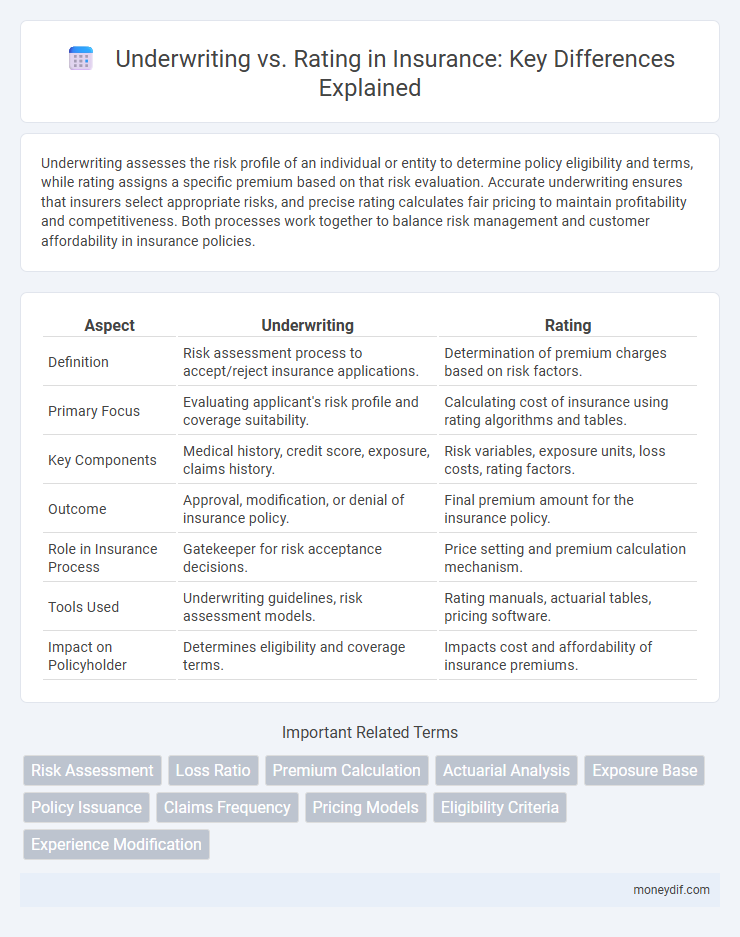

Underwriting assesses the risk profile of an individual or entity to determine policy eligibility and terms, while rating assigns a specific premium based on that risk evaluation. Accurate underwriting ensures that insurers select appropriate risks, and precise rating calculates fair pricing to maintain profitability and competitiveness. Both processes work together to balance risk management and customer affordability in insurance policies.

Table of Comparison

| Aspect | Underwriting | Rating |

|---|---|---|

| Definition | Risk assessment process to accept/reject insurance applications. | Determination of premium charges based on risk factors. |

| Primary Focus | Evaluating applicant's risk profile and coverage suitability. | Calculating cost of insurance using rating algorithms and tables. |

| Key Components | Medical history, credit score, exposure, claims history. | Risk variables, exposure units, loss costs, rating factors. |

| Outcome | Approval, modification, or denial of insurance policy. | Final premium amount for the insurance policy. |

| Role in Insurance Process | Gatekeeper for risk acceptance decisions. | Price setting and premium calculation mechanism. |

| Tools Used | Underwriting guidelines, risk assessment models. | Rating manuals, actuarial tables, pricing software. |

| Impact on Policyholder | Determines eligibility and coverage terms. | Impacts cost and affordability of insurance premiums. |

Understanding Underwriting in Insurance

Underwriting in insurance evaluates the risk profile of applicants to determine policy eligibility and coverage terms, using detailed analysis of health data, financial status, and past claims history. This process ensures appropriate risk classification, which directly affects premium setting and policy conditions. Effective underwriting balances risk management and competitive pricing, essential for maintaining insurer solvency and customer satisfaction.

What is Insurance Rating?

Insurance rating is the process that determines the premium an insured party must pay based on risk factors such as age, health, location, and coverage type. It uses statistical data and actuarial analysis to assess the likelihood of claims and assign appropriate pricing structures. Accurate rating is essential for balancing risk exposure and maintaining insurer profitability.

Key Differences Between Underwriting and Rating

Underwriting evaluates the risk profile of an applicant by analyzing factors such as age, health, and lifestyle to determine policy eligibility. Rating assigns a premium based on the assessed risk, using statistical models and actuarial data to calculate fair pricing. While underwriting focuses on risk selection and acceptance, rating centers on quantifying that risk into a monetary value.

The Role of Underwriters in Risk Assessment

Underwriters play a crucial role in risk assessment by evaluating the potential risks associated with insuring individuals or entities, using detailed data analysis and industry knowledge to determine policy terms and coverage limits. Their expertise ensures that insurance companies maintain balanced risk portfolios and set appropriate premiums. Accurate underwriting directly influences the effectiveness of the rating process, which translates assessed risks into financially viable insurance rates.

How Rating Determines Insurance Premiums

Rating in insurance is the process that determines the cost of premiums by evaluating risk factors such as age, health, location, and coverage limits. Underwriting assesses the risk profile of applicants, but rating translates this assessment into a precise premium amount through statistical models and rate tables. Accurate rating ensures premiums reflect the insured's risk level, maintaining insurer profitability and market competitiveness.

The Underwriting Process: Steps and Criteria

The underwriting process in insurance involves evaluating risks through detailed criteria such as applicant's age, health, occupation, and financial history to determine policy eligibility. Underwriters analyze data from medical records, credit reports, and past claims to customize coverage limits and premiums accurately. This systematic risk assessment ensures the insurer's portfolio remains profitable while providing fair rates to policyholders.

Factors Influencing Insurance Rating Systems

Insurance rating systems depend on factors such as risk assessment, claim history, coverage limits, and policyholder demographics to determine premium costs accurately. Underwriting evaluates the risk profile of applicants by analyzing these data points, including health records, credit scores, and prior claims, to decide eligibility and terms. The interplay between underwriting judgments and rating criteria ensures fair pricing aligned with the insurer's risk exposure and regulatory standards.

Technology’s Impact on Underwriting and Rating

Technology has revolutionized underwriting by integrating artificial intelligence and machine learning algorithms to analyze vast datasets, enabling more accurate risk assessments. In rating, advanced analytics facilitate dynamic pricing models that adjust premiums in real-time based on individual risk factors and market trends. These innovations enhance efficiency, reduce human error, and improve the precision of insurance product offerings.

Common Challenges in Underwriting vs. Rating

Underwriting faces challenges in accurately assessing risk due to incomplete or inconsistent applicant information, leading to potential misclassification or coverage gaps. Rating struggles with creating precise pricing models that balance competitive premiums and profitability while integrating complex risk factors and market fluctuations. Both processes require advanced data analytics and continuous refinement to mitigate underwriting errors and rating inaccuracies effectively.

Why Both Underwriting and Rating Matter to Policyholders

Underwriting evaluates an applicant's risk by analyzing individual factors such as age, health, and occupation, ensuring personalized risk assessment. Rating determines the premium amount based on statistical data and risk categories, providing a fair pricing framework. Both underwriting and rating are crucial for policyholders to receive tailored coverage at competitive rates, balancing protection with affordability.

Important Terms

Risk Assessment

Risk assessment in underwriting involves evaluating an applicant's overall risk profile to determine insurability and policy terms, while rating focuses on quantifying that risk numerically to establish appropriate premiums. Accurate risk assessment ensures underwriting decisions are aligned with rating models, optimizing both risk management and pricing accuracy in insurance policies.

Loss Ratio

Loss ratio measures the proportion of claims paid to earned premiums, serving as a key indicator in underwriting to assess risk selection quality. Rating influences loss ratio by determining premium adequacy, balancing underwriting results to maintain profitability and competitive pricing.

Premium Calculation

Premium calculation in insurance involves underwriting assessing the risk profile of an applicant to determine eligibility and coverage terms, while rating assigns a specific monetary value based on statistical data and risk factors. Underwriting influences premium adjustments by evaluating individual risk characteristics, whereas rating uses predefined algorithms and tables to quantitatively calculate the final premium amount.

Actuarial Analysis

Actuarial analysis in underwriting involves evaluating risk factors to determine the likelihood of a claim, whereas rating focuses on quantifying that risk into precise pricing models for insurance policies. Both processes leverage statistical data and predictive algorithms to optimize risk assessment and premium accuracy within insurance operations.

Exposure Base

Exposure base in underwriting and rating serves as the quantitative measure used to determine policy pricing, reflecting the level of risk associated with insured entities. Accurate identification and analysis of exposure bases such as payroll, vehicle count, or property value are crucial for setting appropriate premiums and mitigating potential losses.

Policy Issuance

Policy issuance involves finalizing and delivering an insurance contract based on underwriting evaluations, which assess risk factors, while rating focuses on determining appropriate premiums using statistical data and risk classifications. Underwriting ensures the acceptability of risk, whereas rating quantifies that risk to set a fair price for the policyholder.

Claims Frequency

Claims frequency serves as a critical metric in underwriting to assess risk by estimating the likelihood of policyholders filing claims, influencing the selection and approval of applicants. Rating models use claims frequency data to adjust premiums accurately, reflecting the anticipated claim occurrences and ensuring pricing aligns with risk levels.

Pricing Models

Underwriting pricing models assess individual risk factors such as health history, lifestyle, and financial status to determine policy eligibility and premiums, while rating models use statistical data and actuarial tables to calculate standardized premium rates based on broader risk categories. Both approaches aim to balance risk and profitability, with underwriting providing personalized pricing and rating ensuring consistency across policyholders.

Eligibility Criteria

Eligibility criteria in underwriting focus on assessing risk factors such as age, health, and financial stability to determine whether an applicant qualifies for coverage, while rating involves calculating premiums based on those risk assessments and other variables like coverage amount and policy type. Underwriting eligibility ensures applicants meet predefined standards, whereas rating quantifies the level of risk to assign appropriate pricing.

Experience Modification

Experience Modification, or Mod, is a critical factor in underwriting as it adjusts risk assessment based on an employer's actual loss history compared to industry averages. In rating, Experience Modification directly influences premium calculations by modifying the base rate to reflect the insured's unique claims experience.

Underwriting vs Rating Infographic