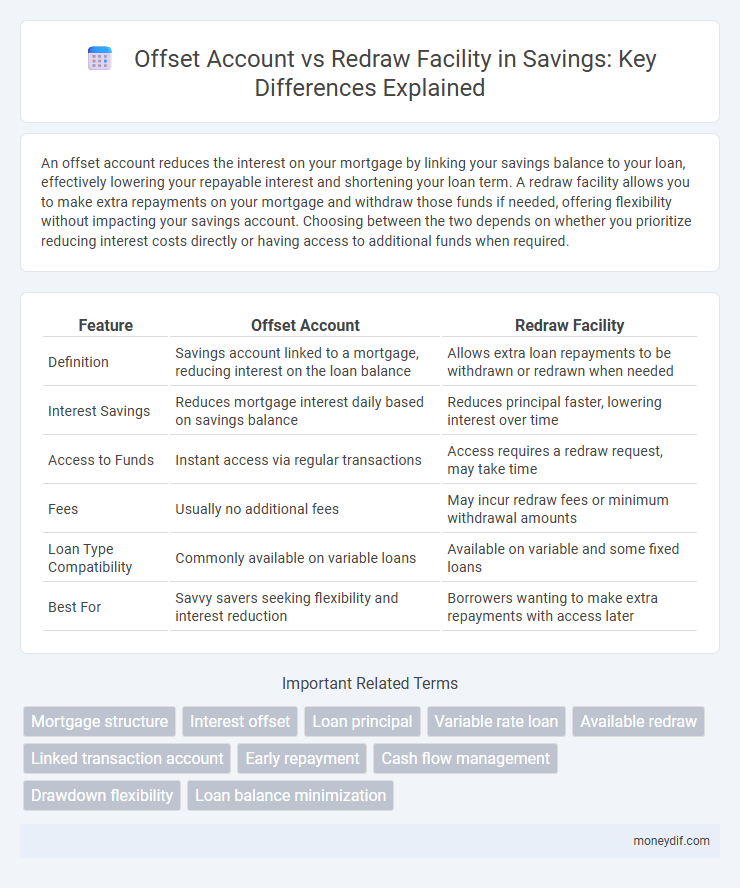

An offset account reduces the interest on your mortgage by linking your savings balance to your loan, effectively lowering your repayable interest and shortening your loan term. A redraw facility allows you to make extra repayments on your mortgage and withdraw those funds if needed, offering flexibility without impacting your savings account. Choosing between the two depends on whether you prioritize reducing interest costs directly or having access to additional funds when required.

Table of Comparison

| Feature | Offset Account | Redraw Facility |

|---|---|---|

| Definition | Savings account linked to a mortgage, reducing interest on the loan balance | Allows extra loan repayments to be withdrawn or redrawn when needed |

| Interest Savings | Reduces mortgage interest daily based on savings balance | Reduces principal faster, lowering interest over time |

| Access to Funds | Instant access via regular transactions | Access requires a redraw request, may take time |

| Fees | Usually no additional fees | May incur redraw fees or minimum withdrawal amounts |

| Loan Type Compatibility | Commonly available on variable loans | Available on variable and some fixed loans |

| Best For | Savvy savers seeking flexibility and interest reduction | Borrowers wanting to make extra repayments with access later |

Understanding Offset Accounts and Redraw Facilities

Offset accounts reduce the interest payable on a mortgage by linking a transaction account to the loan balance, effectively lowering the principal on which interest is calculated. Redraw facilities allow borrowers to access extra repayments made on their mortgage, providing flexibility to withdraw surplus funds if needed. Both offer strategic ways to manage mortgage repayments and optimize savings, but offset accounts provide immediate interest savings while redraw facilities depend on prior extra payments.

How Offset Accounts Work

Offset accounts work by linking a savings or transaction account to your home loan, reducing the loan's interest-bearing balance by the amount of money in the offset account. Funds in the offset account do not earn interest but effectively reduce the principal on which interest is calculated, lowering monthly repayments and the total interest paid over the loan term. This dynamic helps homeowners save on mortgage interest without restricting access to their funds.

How Redraw Facilities Function

Redraw facilities allow borrowers to withdraw extra payments made on their home loan, effectively reducing interest costs by lowering the loan balance. These withdrawals act like a flexible savings tool within the mortgage, enabling access to funds without the need for a separate account. Unlike offset accounts, redraws typically require requests and may have withdrawal limits or fees, impacting overall convenience and liquidity.

Key Differences Between Offset and Redraw Options

An offset account reduces the mortgage principal by linking a savings account to the home loan, effectively lowering interest charges without withdrawing funds. A redraw facility allows borrowers to make extra repayments on their mortgage and access these funds when needed, providing flexibility but potentially affecting interest savings. Key differences include immediate interest reduction through offset accounts versus actual repayment access with redraw facilities, impacting loan management strategies and cash flow control.

Pros and Cons of Offset Accounts

Offset accounts reduce interest on home loans by linking a transaction account to the mortgage balance, lowering overall interest payments and shortening loan terms. These accounts offer flexible access to funds without affecting loan repayments but usually require higher minimum balances and may come with increased fees. However, offset accounts do not accumulate interest themselves, which could be a downside compared to earning interest in separate savings accounts or using redraw facilities.

Advantages and Disadvantages of Redraw Facilities

Redraw facilities allow borrowers to access extra mortgage repayments, offering flexibility to manage cash flow and reduce interest costs by making additional payments. However, disadvantages include possible fees for accessing funds, restrictions on minimum withdrawal amounts, and the risk of reducing the buffer against future financial hardship. Compared to offset accounts, redraw facilities may lack instantaneous access and day-to-day transaction convenience, but provide disciplined debt reduction by limiting frequent withdrawals.

Tax Implications: Offset vs Redraw

An offset account reduces the interest on a mortgage by linking savings directly to the loan balance, effectively lowering taxable interest deductions since the interest expense decreases. Conversely, a redraw facility involves repaying extra mortgage payments and withdrawing them later, maintaining higher reported interest expenses that may offer greater tax deductibility for investment loans. Understanding the differing tax implications between offset accounts and redraw facilities is crucial for optimizing after-tax returns in mortgage management strategies.

Accessibility and Flexibility Compared

An offset account offers immediate access to funds by linking directly to your mortgage, allowing you to reduce interest without extra withdrawals or fees. A redraw facility provides flexibility to withdraw extra repayments made on your loan, but access can sometimes involve restrictions or fees imposed by lenders. Both options enhance savings by lowering mortgage interest, but offset accounts generally deliver superior accessibility and seamless fund management.

Choosing the Best Option for Your Savings Goals

An offset account directly reduces the interest on your mortgage by linking your savings balance to your loan, making it ideal for those wanting immediate interest savings without restrictions. A redraw facility allows you to access extra repayments made on your home loan, offering flexibility but often with access conditions and potential fees. Evaluating your savings goals, liquidity needs, and loan terms helps determine if the offset account's constant interest reduction or the redraw facility's accessibility better supports your financial strategy.

Frequently Asked Questions: Offset Account vs Redraw Facility

An offset account reduces the interest payable on a mortgage by linking a transaction account to the loan balance, effectively lowering the principal on which interest is calculated. A redraw facility allows borrowers to access any extra repayments made towards their home loan, providing flexibility to withdraw funds if needed. Many borrowers ask about fees, accessibility, and interest benefits when choosing between an offset account and a redraw facility for managing mortgage repayments.

Important Terms

Mortgage structure

Mortgage structures with an Offset Account link a savings or transaction account to the loan balance, reducing interest by offsetting deposited funds against the mortgage principal daily. In contrast, a Redraw Facility allows borrowers to withdraw extra repayments made beyond the minimum required, giving flexibility but typically without the daily interest offset benefit of an Offset Account.

Interest offset

Interest offset reduces loan interest by linking a transaction account balance to the mortgage, decreasing daily interest calculations without affecting principal repayments; in contrast, a redraw facility allows borrowers to withdraw extra repayments made beyond the minimum, providing liquidity while potentially reducing interest paid over time. Offset accounts typically offer greater flexibility for day-to-day transactions, whereas redraw facilities tie access to surplus funds directly to the loan balance.

Loan principal

Loan principal can be effectively managed using either an offset account or a redraw facility, both of which reduce interest costs by minimizing the outstanding loan balance. An offset account directly lowers the principal on which interest is calculated by linking a savings or transaction account to the loan, while a redraw facility allows borrowers to withdraw extra repayments made above the minimum principal, providing flexibility without permanently reducing the loan balance.

Variable rate loan

A variable rate loan with an offset account allows borrowers to reduce interest payable by linking transaction funds to the loan balance, effectively lowering daily interest calculation without withdrawing money. In contrast, a redraw facility permits borrowers to access extra repayments made on the variable rate loan, offering flexibility but potentially reducing the loan principal and interest savings compared to an offset account.

Available redraw

An available redraw feature allows borrowers to access extra repayments made on their loan, similar to an offset account that reduces interest by linking to the home loan balance. While an offset account provides flexibility by directly reducing the loan principal daily, a redraw facility requires intentional withdrawal of surplus funds, often with potential fees or restrictions.

Linked transaction account

A linked transaction account offers seamless access to funds and immediate use for daily transactions, while an offset account reduces mortgage interest by linking the balance directly against the loan principal; a redraw facility allows borrowers to withdraw extra repayments made on their mortgage, providing flexible access to surplus funds without affecting their credit limit. Both offset accounts and redraw facilities help minimize interest payments, but offset accounts provide instant transaction capabilities unlike most redraw options.

Early repayment

Early repayment on a home loan with an offset account reduces the interest charged by lowering the loan balance on which interest is calculated without altering the principal, whereas using a redraw facility involves making extra repayments that can be withdrawn later, potentially affecting loan flexibility but not interest savings as immediately as an offset account. Borrowers prioritizing interest reduction benefit more from offset accounts, while those seeking access to extra repayments prefer redraw facilities.

Cash flow management

Effective cash flow management hinges on understanding the distinctions between Offset Accounts and Redraw Facilities: Offset Accounts reduce interest by linking savings to the mortgage balance, enhancing daily interest savings, while Redraw Facilities allow borrowers to withdraw previously paid extra repayments, providing flexible access to funds. Utilizing an Offset Account directly lowers the loan principal on which interest is calculated, whereas Redraw Facilities offer liquidity but may involve withdrawal restrictions or fees, impacting overall loan costs and cash flow dynamics.

Drawdown flexibility

Drawdown flexibility in home loans allows borrowers to access extra repayments either through an offset account, which reduces the loan principal's interest daily, or a redraw facility, enabling withdrawal of surplus payments after minimum requirements are met. Offset accounts offer immediate interest savings by linking to a transaction account, while redraw facilities typically require formal requests and may have fees, affecting the ease and cost of accessing extra funds.

Loan balance minimization

Offset accounts reduce loan balance by directly linking savings to the mortgage, effectively lowering interest calculations daily, while redraw facilities allow borrowers to access extra repayments but do not reduce the principal for interest purposes until paid down. Using an offset account consistently optimizes interest savings and loan balance minimization more efficiently compared to relying solely on a redraw facility.

Offset Account vs Redraw Facility Infographic