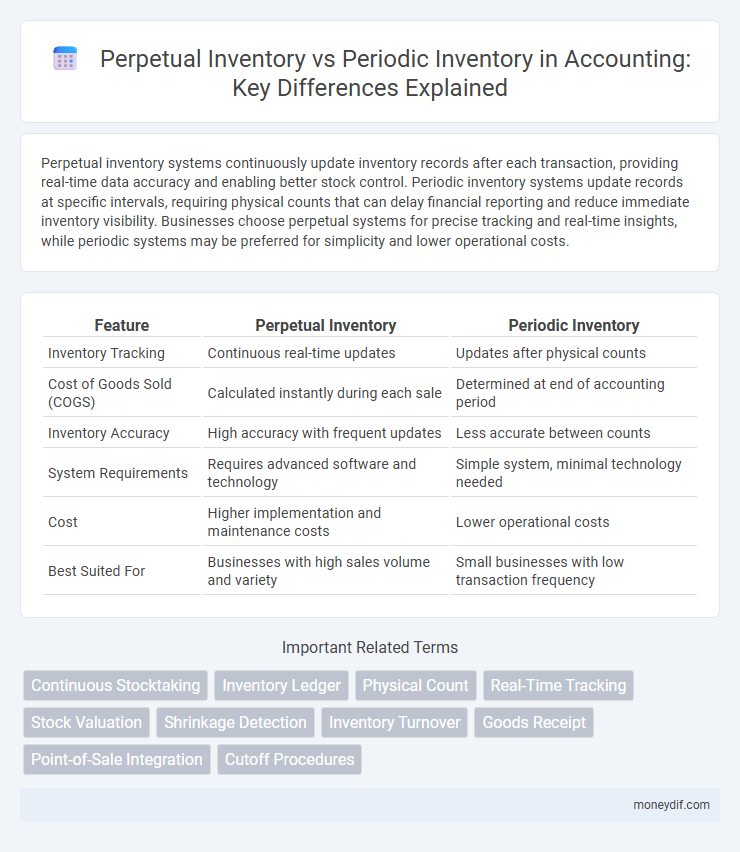

Perpetual inventory systems continuously update inventory records after each transaction, providing real-time data accuracy and enabling better stock control. Periodic inventory systems update records at specific intervals, requiring physical counts that can delay financial reporting and reduce immediate inventory visibility. Businesses choose perpetual systems for precise tracking and real-time insights, while periodic systems may be preferred for simplicity and lower operational costs.

Table of Comparison

| Feature | Perpetual Inventory | Periodic Inventory |

|---|---|---|

| Inventory Tracking | Continuous real-time updates | Updates after physical counts |

| Cost of Goods Sold (COGS) | Calculated instantly during each sale | Determined at end of accounting period |

| Inventory Accuracy | High accuracy with frequent updates | Less accurate between counts |

| System Requirements | Requires advanced software and technology | Simple system, minimal technology needed |

| Cost | Higher implementation and maintenance costs | Lower operational costs |

| Best Suited For | Businesses with high sales volume and variety | Small businesses with low transaction frequency |

Introduction to Inventory Systems

Perpetual inventory systems continuously update inventory records after each transaction, providing real-time data on stock levels and cost of goods sold. Periodic inventory systems, in contrast, update inventory balances only at specific intervals through physical counts, which can delay insights into inventory status. Understanding these systems is crucial for accurate inventory management, financial reporting, and operational control in accounting.

Overview of Perpetual Inventory

Perpetual inventory systems continuously update inventory records through real-time data entry of purchases and sales, ensuring accurate stock levels and immediate detection of discrepancies. This method leverages barcode scanning and integrated accounting software, facilitating precise cost of goods sold calculations and improved financial reporting. Its ongoing inventory tracking contrasts with periodic systems that update only at specified intervals, offering enhanced operational control and timely decision-making for businesses.

Overview of Periodic Inventory

Periodic inventory systems update stock records and cost of goods sold at specific intervals, such as monthly or annually, rather than continuously. This method involves physically counting inventory at the end of the period to determine the quantity on hand and calculate costs. Periodic inventory is often preferred by small businesses with simpler inventory management needs due to its lower operational complexity compared to perpetual systems.

Key Differences Between Perpetual and Periodic Inventory

Perpetual inventory systems record inventory changes continuously with each transaction, providing real-time data on stock levels and cost of goods sold (COGS). Periodic inventory systems update inventory balances at specific intervals, relying on physical counts to determine COGS, which can delay financial reporting accuracy. The perpetual method is preferable for businesses needing precise inventory tracking, while the periodic system suits simpler operations with less frequent inventory assessments.

Advantages of Perpetual Inventory

Perpetual inventory systems provide real-time inventory tracking and accurate stock level updates, enhancing the efficiency of order management and reducing the risk of stockouts or overstocking. This method allows for immediate detection of inventory discrepancies and supports better decision-making through continuous data availability. Businesses benefit from improved financial reporting accuracy and streamlined audit processes with perpetual inventory systems.

Advantages of Periodic Inventory

Periodic inventory provides a simple and cost-effective method for small businesses to track inventory levels without the need for sophisticated technology or continuous monitoring. It allows for easier implementation and fewer resources required for record-keeping compared to perpetual inventory systems. This method also facilitates physical verification and reduces the risk of discrepancies caused by system errors or theft.

Limitations of Perpetual Inventory

Perpetual inventory systems face limitations such as high implementation and maintenance costs due to the need for sophisticated software and hardware. They may also encounter inaccuracies in real-time inventory tracking caused by theft, spoilage, or human error during data entry. Furthermore, these systems require continuous updates and staff training, which can strain resources in smaller accounting operations.

Limitations of Periodic Inventory

Periodic inventory systems often result in less accurate inventory records due to the infrequent updates, increasing the risk of stockouts or overstock situations. This method relies on physical counts that can be time-consuming and prone to human error, leading to discrepancies in financial reporting. Unlike perpetual inventory systems, periodic systems lack real-time tracking, which impairs timely decision-making and efficient inventory management.

Choosing the Right Inventory System for Your Business

Selecting the appropriate inventory system depends on the nature and scale of your business operations; perpetual inventory systems provide real-time tracking of stock levels and streamline accounting with continuous updates, ideal for businesses requiring precise inventory control. Periodic inventory systems record inventory at specific intervals, which may suit smaller businesses with less frequent stock changes or simpler accounting needs. Understanding the trade-offs in accuracy, cost, and operational complexity helps businesses align their inventory management approach with their financial reporting and operational efficiency goals.

Impact on Financial Statements and Reporting

Perpetual inventory systems provide real-time data on inventory levels and cost of goods sold, resulting in more accurate and timely financial statements. Periodic inventory systems update inventory and expense accounts only at the end of an accounting period, which can delay recognition of inventory discrepancies and affect the accuracy of income statements. The choice between perpetual and periodic inventory impacts the balance sheet's inventory valuation and the income statement's reported profitability.

Important Terms

Continuous Stocktaking

Continuous stocktaking ensures accurate perpetual inventory management by updating stock levels in real-time, unlike periodic inventory which relies on scheduled physical counts.

Inventory Ledger

The inventory ledger records real-time stock changes in perpetual inventory systems, while periodic inventory updates occur only at the end of accounting periods.

Physical Count

Physical count is a crucial process for verifying inventory accuracy by physically counting stock on hand, serving as a key control in both perpetual and periodic inventory systems. In perpetual inventory systems, physical counts reconcile ongoing digital records with actual stock, while in periodic systems, they are essential for determining ending inventory and calculating cost of goods sold at specific intervals.

Real-Time Tracking

Real-time tracking in perpetual inventory systems enables continuous updates of stock levels and accurate data for decision-making, unlike periodic inventory which relies on less frequent physical counts.

Stock Valuation

Stock valuation accuracy is enhanced by perpetual inventory systems through real-time tracking, whereas periodic inventory requires end-of-period counts, potentially affecting cost of goods sold calculations.

Shrinkage Detection

Shrinkage detection in perpetual inventory systems benefits from real-time tracking of stock levels through barcode scanning and RFID technology, enabling immediate identification of discrepancies caused by theft, damage, or errors. In contrast, periodic inventory systems rely on physical counts at set intervals, making shrinkage detection slower and less precise, often resulting in delayed responses to inventory loss.

Inventory Turnover

Inventory turnover is typically higher and more accurately tracked using a perpetual inventory system compared to a periodic inventory system due to real-time inventory updates.

Goods Receipt

Goods receipt updates inventory immediately in perpetual inventory systems, while in periodic inventory systems, it is recorded separately and inventory levels are adjusted only at period-end.

Point-of-Sale Integration

Point-of-Sale integration enables real-time tracking and automatic updates of perpetual inventory, contrasting with periodic inventory systems that require manual stock counts at specific intervals.

Cutoff Procedures

Cutoff procedures ensure accurate accounting by verifying that all inventory transactions are recorded in the correct accounting period, playing a critical role in reconciling perpetual inventory systems that update continuously with periodic inventory systems that record inventory only at specific intervals.

perpetual inventory vs periodic inventory Infographic