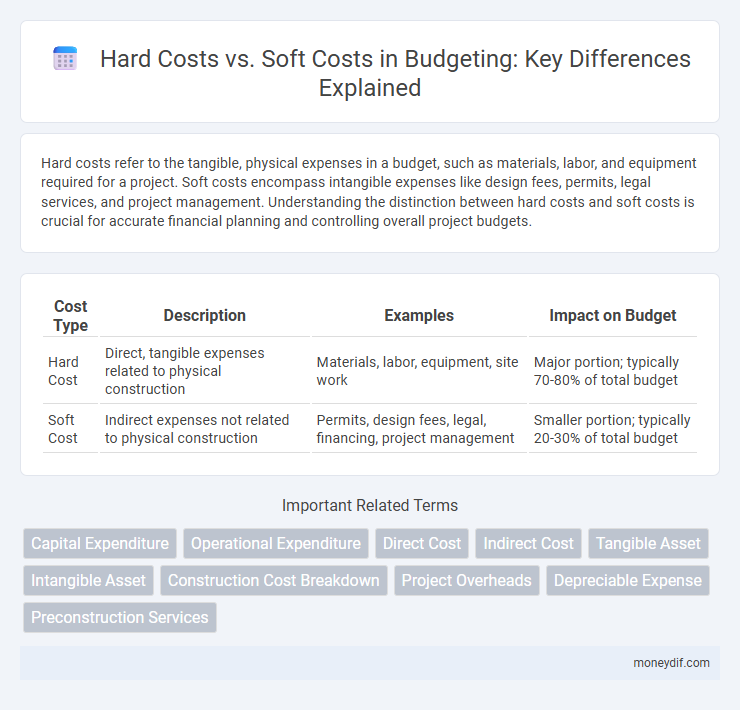

Hard costs refer to the tangible, physical expenses in a budget, such as materials, labor, and equipment required for a project. Soft costs encompass intangible expenses like design fees, permits, legal services, and project management. Understanding the distinction between hard costs and soft costs is crucial for accurate financial planning and controlling overall project budgets.

Table of Comparison

| Cost Type | Description | Examples | Impact on Budget |

|---|---|---|---|

| Hard Cost | Direct, tangible expenses related to physical construction | Materials, labor, equipment, site work | Major portion; typically 70-80% of total budget |

| Soft Cost | Indirect expenses not related to physical construction | Permits, design fees, legal, financing, project management | Smaller portion; typically 20-30% of total budget |

Understanding Hard Costs and Soft Costs

Hard costs refer to the tangible, physical expenses involved in construction projects, including materials, labor, and equipment necessary for building structures. Soft costs encompass non-physical expenses like architectural fees, permits, legal services, and project management, which support the development process without contributing to the physical construction. Distinguishing between hard costs and soft costs is essential for accurate budgeting and financial planning in construction and development projects.

Key Differences Between Hard and Soft Costs

Hard costs in a budget refer to tangible, physical expenses such as construction materials, labor, and equipment directly involved in building projects. Soft costs encompass intangible expenses like architectural fees, permits, insurance, and administrative expenses that support the project's development but do not include physical construction elements. The key difference lies in hard costs being fixed and measurable construction inputs, while soft costs cover indirect, variable expenses essential for project planning and management.

Examples of Hard Costs in Budgeting

Hard costs in budgeting refer to tangible, physical expenses directly associated with construction or production, such as materials, labor, and equipment. Examples include concrete, steel, roofing, flooring, and contractor fees, all of which contribute to the physical structure of a project. Understanding these hard costs is essential for accurate financial planning and cost control in construction and manufacturing budgets.

Examples of Soft Costs in Budget Planning

Soft costs in budget planning encompass expenses such as architectural and engineering fees, permits and inspection charges, and legal and consulting services. These costs also include project management salaries, insurance premiums, and financing fees, which do not directly involve physical construction. Accurately estimating soft costs ensures comprehensive budgeting and prevents unexpected financial shortfalls during project execution.

Why Distinguishing Costs Matters in Budget Management

Distinguishing hard costs from soft costs is crucial for accurate budget management because hard costs involve tangible expenses like materials and labor, while soft costs cover intangible expenses such as design fees, permits, and administrative costs. Properly categorizing these costs enables precise financial tracking, reduces the risk of overruns, and ensures better resource allocation throughout a project. Understanding these distinctions helps stakeholders create realistic budgets and make informed decisions that optimize project profitability and timelines.

Hard Cost Impacts on Project Budgets

Hard costs, including materials, labor, and equipment, constitute the largest portion of a project budget and directly impact the overall financial plan. These tangible expenses are often fixed and less flexible, requiring precise estimation to avoid budget overruns. Proper management of hard costs ensures accurate allocation of resources and successful project completion within budget constraints.

Evaluating the Significance of Soft Costs

Soft costs, including architectural fees, permits, and legal expenses, can constitute 20-30% of a construction project's total budget, significantly impacting financial planning. Unlike hard costs, which cover physical construction materials and labor, soft costs often fluctuate based on project complexity and regulatory requirements. Evaluating the significance of soft costs is crucial for accurate budget forecasting and avoiding unexpected overruns.

Strategies to Accurately Estimate Hard and Soft Costs

Accurately estimating hard and soft costs begins with a detailed breakdown of construction materials, labor, and equipment for hard costs, alongside regulatory fees, design fees, and project management expenses for soft costs. Utilizing historical data and market analysis enables precise forecasting of fluctuating prices and labor rates, while software tools enhance cost tracking and adjustment throughout the project lifecycle. Collaborating closely with contractors, architects, and financial experts ensures comprehensive inclusion of all potential expenses, minimizing budget overruns and project delays.

Common Mistakes in Differentiating Cost Types

Misclassifying hard costs, which include tangible expenses like materials and labor, as soft costs, such as permits, design fees, and administrative expenses, often leads to inaccurate budgeting and financial forecasting. Overlooking the distinct nature of hard and soft costs can cause project managers to underestimate contingency funds, resulting in cash flow issues during construction. Clear categorization ensures precise cost tracking, improves budget control, and reduces the risk of overruns in construction project management.

Optimizing Budgets by Balancing Hard and Soft Costs

Optimizing budgets requires a strategic balance between hard costs, such as construction materials and labor, and soft costs, including design fees, permits, and administrative expenses. Prioritizing cost-effective procurement and efficient project management can significantly reduce hard costs, while early engagement with architects and consultants helps minimize soft cost overruns. Careful allocation between tangible assets and intangible services ensures comprehensive budget control and maximizes overall project financial efficiency.

Important Terms

Capital Expenditure

Capital expenditure for construction projects typically divides into hard costs, which cover physical building expenses like materials and labor, and soft costs, which include non-physical expenses such as design fees, permits, and financing.

Operational Expenditure

Operational expenditure includes both hard costs, such as physical assets and infrastructure maintenance, and soft costs, encompassing administrative expenses and professional services.

Direct Cost

Direct costs encompass both hard costs, which include tangible expenses like materials and labor for construction, and soft costs, which cover intangible expenses such as design fees, permits, and administrative expenses.

Indirect Cost

Indirect costs include overhead expenses not directly tied to physical construction, differing from hard costs which cover tangible materials and labor, and soft costs which encompass fees like permits, design, and administrative expenses.

Tangible Asset

Tangible assets primarily contribute to hard costs such as construction materials and labor, while soft costs encompass intangible expenses like design fees and permits.

Intangible Asset

Intangible assets, such as intellectual property and brand value, are often categorized under soft costs, while hard costs primarily encompass tangible expenses like construction and materials.

Construction Cost Breakdown

Construction cost breakdown distinguishes hard costs, including materials and labor, from soft costs such as design fees, permits, and financing expenses.

Project Overheads

Project overheads typically include indirect expenses such as administrative salaries and site utilities, classified as soft costs, while hard costs cover direct construction expenses like materials and labor, both essential for comprehensive budget management.

Depreciable Expense

Depreciable expense primarily applies to hard costs like construction materials and equipment, while soft costs such as architectural fees and permits are generally not depreciable.

Preconstruction Services

Preconstruction services help identify and control hard costs such as materials and labor, and soft costs including design fees and permits, to optimize overall project budgeting.

Hard cost vs Soft cost Infographic