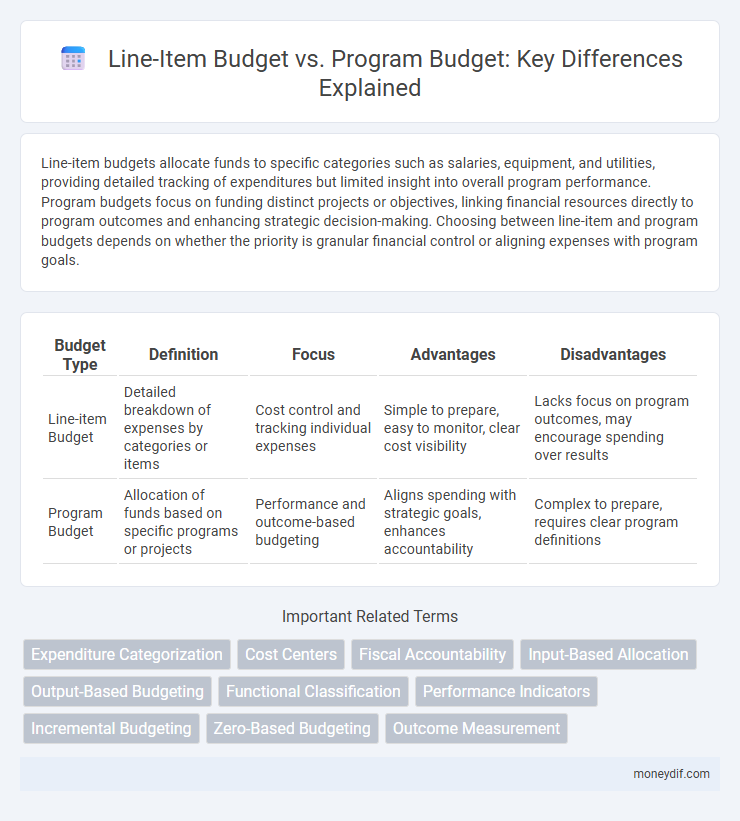

Line-item budgets allocate funds to specific categories such as salaries, equipment, and utilities, providing detailed tracking of expenditures but limited insight into overall program performance. Program budgets focus on funding distinct projects or objectives, linking financial resources directly to program outcomes and enhancing strategic decision-making. Choosing between line-item and program budgets depends on whether the priority is granular financial control or aligning expenses with program goals.

Table of Comparison

| Budget Type | Definition | Focus | Advantages | Disadvantages |

|---|---|---|---|---|

| Line-item Budget | Detailed breakdown of expenses by categories or items | Cost control and tracking individual expenses | Simple to prepare, easy to monitor, clear cost visibility | Lacks focus on program outcomes, may encourage spending over results |

| Program Budget | Allocation of funds based on specific programs or projects | Performance and outcome-based budgeting | Aligns spending with strategic goals, enhances accountability | Complex to prepare, requires clear program definitions |

Introduction to Line-item Budgeting and Program Budgeting

Line-item budgeting allocates funds based on specific expense categories such as salaries, equipment, and supplies, offering detailed tracking and control over individual expenditures. Program budgeting organizes funds according to projects or programs, emphasizing outcomes and performance by linking resources to objectives. Both approaches provide unique frameworks for financial planning, with line-item budgets prioritizing cost control and program budgets focusing on strategic goals.

Key Differences Between Line-item and Program Budgets

Line-item budgets categorize expenses by specific items such as salaries, equipment, and supplies, providing detailed tracking of each cost component. Program budgets allocate resources based on distinct projects or programs, emphasizing overall funding needs and outcomes rather than individual expenditures. Key differences include the line-item budget's focus on cost control and accountability, while the program budget prioritizes strategic allocation to achieve program goals and measure performance.

Advantages of Line-item Budgeting

Line-item budgeting provides clear and detailed tracking of expenses by categorizing costs into specific items, enhancing financial transparency and control. It simplifies the budgeting process, making it easier for organizations to allocate funds, monitor spending, and identify areas of overspending. This method facilitates accountability by allowing straightforward comparisons between budgeted amounts and actual expenditures for each line item.

Advantages of Program Budgeting

Program budgeting enhances resource allocation efficiency by linking expenditures directly to specific goals and outcomes, improving transparency and accountability in financial management. It facilitates better decision-making by providing a comprehensive view of program performance and cost-effectiveness, enabling organizations to prioritize funding based on impact. This method supports strategic planning and performance evaluation, making it easier to adjust budgets in response to changing priorities and measurable results.

Disadvantages of Line-item Budgeting

Line-item budgeting often limits flexibility by allocating funds strictly to specific categories, hindering adaptability to changing organizational priorities or unforeseen expenses. It emphasizes control over spending rather than outcomes, making performance evaluation and resource reallocation challenging. Additionally, this approach can lead to inefficiencies by ignoring program effectiveness and failing to align financial resources with strategic goals.

Disadvantages of Program Budgeting

Program budgeting can obscure detailed cost control by aggregating expenses under broader categories, making it difficult to track specific line-item expenditures. The lack of granular financial data limits accountability and complicates audits, potentially leading to inefficient resource allocation. Moreover, its complexity requires advanced management skills, which can hinder timely decision-making in organizations with limited budgeting expertise.

When to Use Line-item vs. Program Budgets

Line-item budgets are best suited for organizations requiring strict control over specific expenses, such as government agencies or departments with detailed financial reporting needs. Program budgets are ideal when the focus is on funding outcomes or projects, allowing flexible allocation of resources to achieve strategic goals. Selecting between these depends on whether the priority is granular expense tracking or aligning expenditures with program objectives.

Impact on Financial Transparency and Accountability

Line-item budgets enhance financial transparency by detailing specific expenditures, enabling clear tracking and control of funds. Program budgets allocate resources based on activities or outcomes, which supports accountability by linking spending to measurable results. Comparing both, line-item budgets provide granular financial visibility while program budgets promote strategic oversight and outcome-based evaluation.

Real-world Examples of Line-item and Program Budgets

Line-item budgets, commonly used by government agencies such as the U.S. Department of Education, break down expenses into specific categories like salaries, supplies, and equipment, allowing for precise tracking and control of funds. Program budgets, employed by organizations like the World Health Organization, allocate funds based on specific programs or projects, facilitating a focus on outcomes and performance rather than individual expense categories. Real-world examples demonstrate that line-item budgets provide detailed financial oversight, while program budgets promote strategic allocation aligned with organizational goals.

Choosing the Best Budgeting Method for Your Organization

Line-item budgets emphasize detailed tracking of expenses by specific categories, making them ideal for organizations requiring precise cost control and straightforward financial reporting. Program budgets allocate funds based on projects or objectives, fostering alignment between spending and organizational goals while enhancing performance measurement. Selecting the best budgeting method depends on your organization's size, complexity, and strategic priorities, ensuring efficient resource allocation and transparent financial management.

Important Terms

Expenditure Categorization

Expenditure categorization in a line-item budget organizes costs by specific items, such as salaries and materials, enabling detailed tracking and control of expenses. In contrast, a program budget groups expenditures based on activities or objectives, facilitating assessment of financial efficiency and outcomes within distinct programs.

Cost Centers

Cost centers focus on tracking expenses at a granular, operational level, aligning closely with line-item budgets that detail specific cost categories such as salaries, supplies, and utilities. In contrast, program budgets aggregate costs by projects or initiatives, linking expenditures to broader organizational goals and outcomes rather than individual expense items.

Fiscal Accountability

Fiscal accountability improves when government entities adopt line-item budgeting for precise expenditure tracking, while program budgeting enhances accountability by linking funds directly to measurable outcomes and objectives. Comparing both, line-item budgets emphasize financial control over specific expenses, whereas program budgets prioritize efficiency and effectiveness in achieving policy goals.

Input-Based Allocation

Input-Based Allocation focuses on distributing resources according to specific inputs such as personnel, equipment, and materials, typically aligned with a Line-item Budget that details these individual expenses. In contrast, Program Budget allocates funds based on overarching objectives and program outcomes, emphasizing the effectiveness of resource use rather than just the itemized inputs.

Output-Based Budgeting

Output-Based Budgeting focuses on linking financial resources directly to measurable results, enhancing accountability and efficiency compared to traditional Line-item Budgeting, which emphasizes expenditure categories without clear performance metrics. Unlike Line-item Budgeting, Program Budgeting allocates funds based on specific programs or projects, aligning budgetary decisions with targeted outcomes and enabling better evaluation of government or organizational effectiveness.

Functional Classification

Functional classification categorizes budget expenditures based on government functions or services, allowing better alignment with program objectives and outcomes, whereas line-item budgets focus on specific expense categories such as salaries and supplies. Program budgets integrate functional classification to allocate resources effectively across different government programs by linking expenditures directly to the functions and results they aim to achieve.

Performance Indicators

Performance indicators for line-item budgets focus on tracking expenditures against specific cost categories, ensuring precise cost control and compliance with allocated funds. In contrast, program budget performance indicators measure outcomes and effectiveness by evaluating resource utilization relative to program goals and overall impact.

Incremental Budgeting

Incremental budgeting adjusts previous budgets by small amounts, often leading to incremental increases in line-item budgets focused on specific expense categories rather than program outcomes. In contrast, program budgeting allocates funds based on objectives and performance, emphasizing cost-effectiveness and measurable results over incremental changes in individual line items.

Zero-Based Budgeting

Zero-Based Budgeting (ZBB) requires justifying all expenses from scratch, contrasting with line-item budgeting that allocates funds based on previous expenditures. Program budgeting, aligned with ZBB principles, focuses on funding specific outcomes and activities, enhancing resource efficiency and strategic goal alignment.

Outcome Measurement

Outcome measurement evaluates the effectiveness of expenditures, providing critical insights into whether program budgets achieve specified objectives compared to line-item budgets focused solely on financial inputs. Program budgeting aligns resources with strategic goals and facilitates performance tracking, while line-item budgets primarily emphasize cost control without directly linking spending to measurable results.

Line-item Budget vs Program Budget Infographic