Performance budgeting allocates resources based on measurable results and outcomes, enhancing accountability and efficiency in public spending. Formula budgeting distributes funds according to predetermined criteria or formulas, ensuring consistency and predictability across departments or programs. Choosing between the two depends on the need for flexibility in addressing specific goals versus maintaining standardized funding allocations.

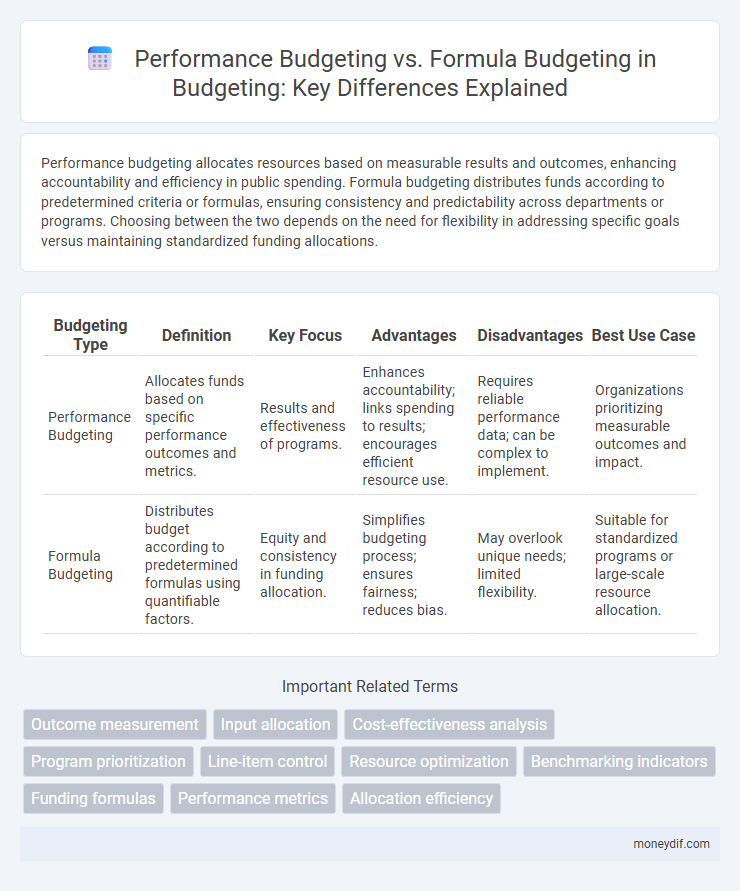

Table of Comparison

| Budgeting Type | Definition | Key Focus | Advantages | Disadvantages | Best Use Case |

|---|---|---|---|---|---|

| Performance Budgeting | Allocates funds based on specific performance outcomes and metrics. | Results and effectiveness of programs. | Enhances accountability; links spending to results; encourages efficient resource use. | Requires reliable performance data; can be complex to implement. | Organizations prioritizing measurable outcomes and impact. |

| Formula Budgeting | Distributes budget according to predetermined formulas using quantifiable factors. | Equity and consistency in funding allocation. | Simplifies budgeting process; ensures fairness; reduces bias. | May overlook unique needs; limited flexibility. | Suitable for standardized programs or large-scale resource allocation. |

Introduction to Performance and Formula Budgeting

Performance budgeting allocates funds based on measurable results and outcomes, enhancing accountability by linking expenditures directly to program performance. Formula budgeting distributes resources according to predetermined criteria or formulas, ensuring consistency and fairness in fund allocation across departments or regions. Both methods aim to improve budget efficiency but differ in focus--performance budgeting targets effectiveness, while formula budgeting emphasizes equity and standardization.

Key Principles of Performance Budgeting

Performance budgeting emphasizes allocating funds based on measurable outcomes and efficiency, ensuring resources directly support program goals and improve service delivery. It involves establishing clear performance indicators and linking expenditures to results, enhancing accountability and strategic decision-making. The approach prioritizes evaluating effectiveness and cost-efficiency to optimize budget utilization and achieve targeted objectives.

Core Concepts of Formula Budgeting

Formula budgeting allocates funds based on predetermined criteria such as population, enrollment, or workload, ensuring objectivity and consistency. It relies on quantitative formulas to distribute resources, minimizing discretion and promoting equity across departments or programs. Core concepts include transparency, predictability, and alignment with measurable indicators to support efficient fiscal planning.

Differences Between Performance and Formula Budgeting

Performance budgeting allocates funds based on measurable outcomes and the efficiency of producing public services, emphasizing accountability and results. Formula budgeting distributes resources using predetermined criteria or formulas, such as population size or service demand, ensuring predictable and equitable allocation. The main difference lies in performance budgeting's focus on evaluating effectiveness, while formula budgeting prioritizes standardized, needs-based distribution.

Advantages of Performance Budgeting

Performance budgeting enhances resource allocation by linking funding directly to measurable outcomes and program efficiency. This approach increases accountability through clear performance indicators and improves decision-making based on empirical evidence. Government agencies adopting performance budgeting often experience improved transparency and more effective use of public funds compared to formula budgeting.

Benefits of Formula Budgeting

Formula budgeting streamlines resource allocation by using objective, data-driven criteria such as population size or service needs, enhancing transparency and fairness in budget distribution. It simplifies the budgeting process, reducing administrative overhead and enabling quicker adjustments based on quantifiable indicators. This method promotes consistency and predictability in funding, supporting better planning and accountability in public financial management.

Challenges in Implementing Performance Budgeting

Performance budgeting faces challenges such as accurately defining measurable outcomes and aligning them with organizational goals, which complicates resource allocation. Unlike formula budgeting, which relies on predetermined formulas for fund distribution, performance budgeting requires continuous data collection and analysis, increasing administrative burden. This complexity often leads to resistance from stakeholders accustomed to simpler, rule-based formula budgeting methods.

Limitations of Formula Budgeting Practices

Formula budgeting often lacks flexibility by rigidly allocating funds based on preset criteria, which may not reflect current organizational needs or priorities. It can overlook qualitative factors and unique situational variables, leading to inefficient resource distribution. This method may also inhibit responsiveness to changing economic conditions or policy goals, limiting its effectiveness in dynamic environments.

Choosing the Right Budgeting Approach for Organizations

Performance budgeting emphasizes linking budget allocations directly to measurable outcomes and program efficiency, enabling organizations to optimize resource use based on results. Formula budgeting relies on predetermined criteria such as population size or historical expenditure patterns, offering simplicity and predictability but less flexibility in addressing unique organizational needs. Organizations should evaluate factors like operational complexity, accountability requirements, and available data to select a budgeting approach that aligns with strategic goals and enhances financial management.

Future Trends in Budgeting Methodologies

Performance budgeting emphasizes outcome-based allocations that enhance transparency and accountability by linking expenditures directly to measurable results. Formula budgeting uses predetermined algorithms to distribute funds, ensuring consistency and predictability but potentially limiting flexibility in addressing unique program needs. Emerging trends point toward hybrid models integrating artificial intelligence and real-time data analytics to optimize budget accuracy and responsiveness, fostering adaptive resource management aligned with dynamic organizational goals.

Important Terms

Outcome measurement

Outcome measurement in performance budgeting focuses on evaluating the actual results and effectiveness of programs by linking expenditures to specific outcomes, enhancing accountability. Formula budgeting allocates resources based on predetermined criteria or formulas, often emphasizing inputs rather than measurable results, which can limit detailed outcome assessment.

Input allocation

Input allocation in performance budgeting focuses on distributing resources based on achieving specific outcomes and efficiency indicators, optimizing program impact through measurable results. Formula budgeting allocates inputs using predefined criteria such as population size or historical expenditure, promoting standardized funding but potentially limiting responsiveness to performance variations.

Cost-effectiveness analysis

Cost-effectiveness analysis evaluates the economic efficiency of performance budgeting by linking financial resources directly to measurable outcomes, whereas formula budgeting allocates funds based on predetermined formulas without explicit performance metrics. Performance budgeting typically offers greater transparency and accountability in resource utilization compared to formula budgeting, which prioritizes standardized distribution over outcome-based assessment.

Program prioritization

Program prioritization aligns with performance budgeting by allocating resources based on measurable outcomes and efficiency, ensuring funds target high-impact initiatives. In contrast, formula budgeting distributes resources according to predetermined criteria or formulas, often lacking the flexibility to respond to changing program performance metrics.

Line-item control

Line-item control in performance budgeting focuses on detailed tracking of expenditures by specific activities to ensure accountability and efficiency, while formula budgeting allocates resources based on preset formulas tied to workload or population indicators, promoting standardized and equitable funding across programs. Performance budgeting emphasizes outcome-based financial management through line-item scrutiny, whereas formula budgeting relies on data-driven allocation mechanisms without detailed itemized expenditure monitoring.

Resource optimization

Resource optimization through performance budgeting focuses on aligning expenditures with measurable outcomes and key performance indicators, enhancing cost-effectiveness and accountability. In contrast, formula budgeting allocates resources based on predetermined criteria or formulas, potentially sacrificing flexibility and nuanced performance evaluation for standardization and predictability.

Benchmarking indicators

Benchmarking indicators in performance budgeting focus on outcome-based metrics such as cost-efficiency, service quality, and program effectiveness, enabling organizations to evaluate actual results against predefined goals. In contrast, formula budgeting relies on standardized allocation criteria like enrollment numbers or historical expenditures, emphasizing equitable resource distribution rather than direct performance outcomes.

Funding formulas

Performance budgeting allocates funds based on measurable outcomes and efficiency metrics to enhance accountability, while formula budgeting distributes resources using predetermined criteria such as enrollment numbers or population size, ensuring consistency and equity. Funding formulas in formula budgeting rely on data-driven indicators to systematically determine budget amounts, contrasting with the outcome-focused allocation in performance budgeting.

Performance metrics

Performance budgeting focuses on allocating funds based on measurable outcomes and specific objectives, ensuring expenditures align directly with achieved results. Formula budgeting employs predetermined mathematical formulas tied to quantifiable factors like population size or workload, promoting consistency and equity in resource distribution.

Allocation efficiency

Allocation efficiency measures how well resources are distributed to maximize outputs, with performance budgeting focusing on outcomes linked to specific goals, optimizing resource use based on measurable results. Formula budgeting allocates funds according to preset mathematical criteria, which may streamline fairness but can limit adaptive efficiency in responding to changing performance needs.

Performance budgeting vs Formula budgeting Infographic