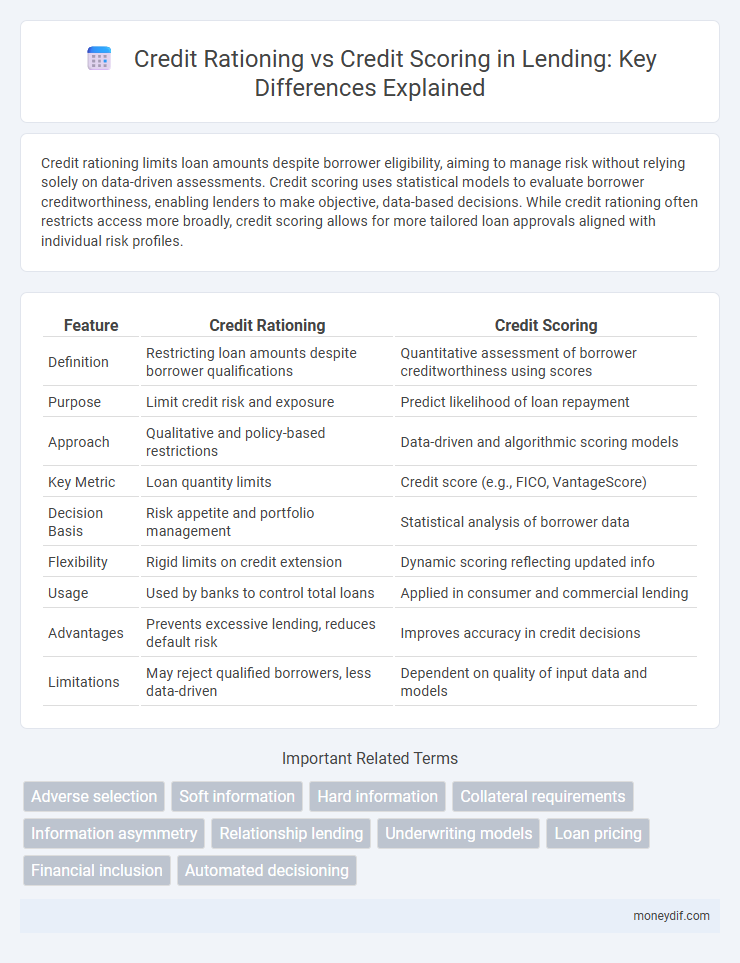

Credit rationing limits loan amounts despite borrower eligibility, aiming to manage risk without relying solely on data-driven assessments. Credit scoring uses statistical models to evaluate borrower creditworthiness, enabling lenders to make objective, data-based decisions. While credit rationing often restricts access more broadly, credit scoring allows for more tailored loan approvals aligned with individual risk profiles.

Table of Comparison

| Feature | Credit Rationing | Credit Scoring |

|---|---|---|

| Definition | Restricting loan amounts despite borrower qualifications | Quantitative assessment of borrower creditworthiness using scores |

| Purpose | Limit credit risk and exposure | Predict likelihood of loan repayment |

| Approach | Qualitative and policy-based restrictions | Data-driven and algorithmic scoring models |

| Key Metric | Loan quantity limits | Credit score (e.g., FICO, VantageScore) |

| Decision Basis | Risk appetite and portfolio management | Statistical analysis of borrower data |

| Flexibility | Rigid limits on credit extension | Dynamic scoring reflecting updated info |

| Usage | Used by banks to control total loans | Applied in consumer and commercial lending |

| Advantages | Prevents excessive lending, reduces default risk | Improves accuracy in credit decisions |

| Limitations | May reject qualified borrowers, less data-driven | Dependent on quality of input data and models |

Understanding Credit Rationing: Definition and Mechanisms

Credit rationing occurs when lenders limit the amount of credit available to borrowers despite their willingness to pay higher interest rates, often due to asymmetric information and the risk of default. Unlike credit scoring, which evaluates borrowers based on quantitative risk models and credit history to approve or deny loans, credit rationing involves denying credit to certain applicants even if they meet lending criteria to minimize adverse selection and moral hazard. This mechanism protects financial institutions from excessive credit risk but can restrict access to capital for potentially creditworthy borrowers.

What Is Credit Scoring? A Modern Approach to Credit Assessment

Credit scoring is a modern approach to credit assessment that uses statistical models to evaluate a borrower's creditworthiness based on quantitative data such as payment history, outstanding debt, and credit utilization. Unlike credit rationing, which involves limiting credit supply due to uncertainty or asymmetric information, credit scoring provides an objective, data-driven method that improves accuracy in risk prediction and decision-making. This approach enhances lenders' ability to extend credit efficiently by minimizing default risks and optimizing portfolio management.

Key Differences Between Credit Rationing and Credit Scoring

Credit rationing limits the amount of credit extended to borrowers regardless of their creditworthiness, often due to lender risk aversion or regulatory constraints, whereas credit scoring evaluates individual borrower credit risk using statistical models to determine eligibility and loan terms. Credit rationing may result in credit denial even for qualified borrowers, while credit scoring enables precise risk assessment and differentiated interest rates based on credit profiles. Understanding these differences is crucial for lenders aiming to balance risk management and market access effectively.

Advantages of Credit Rationing in Lending Practices

Credit rationing limits loan amounts based on borrowers' risk profiles rather than solely relying on credit scores, reducing the likelihood of default by carefully controlling exposure. This approach allows lenders to manage asymmetric information and adverse selection more effectively, ensuring more prudent allocation of credit. By prioritizing qualitative assessments alongside quantitative metrics, credit rationing enhances loan portfolio quality and maintains financial stability.

Benefits of Credit Scoring for Borrowers and Lenders

Credit scoring improves loan approval efficiency by using statistical models to assess borrower risk, enabling lenders to offer fairer interest rates and quicker decisions. Borrowers benefit from increased transparency and access to credit, as their scores provide clear criteria for approval, reducing bias and favoritism. For lenders, credit scoring reduces default rates and operational costs by identifying high-risk applicants, leading to a more stable and profitable credit portfolio.

Limitations and Risks of Credit Rationing

Credit rationing restricts the amount of credit available to borrowers irrespective of their creditworthiness, leading to inefficiencies in capital allocation and potential exclusion of creditworthy applicants. Unlike credit scoring, which uses data-driven algorithms to assess risk, credit rationing relies on subjective judgments that can cause adverse selection and moral hazard. These limitations increase systemic risk by concentrating credit exposure and reducing access for smaller or newer borrowers, ultimately hindering financial market efficiency.

Drawbacks and Challenges of Credit Scoring Systems

Credit scoring systems often struggle with limited data quality and incomplete borrower information, leading to potential inaccuracies in risk assessment. These models can inadvertently perpetuate biases, resulting in unfair credit access and discrimination against certain demographic groups. Furthermore, credit scoring's reliance on historical financial behavior restricts its ability to evaluate emerging borrowers or those with unconventional credit profiles effectively.

Impact on Borrower Accessibility: Rationing vs Scoring

Credit rationing limits borrower accessibility by restricting loan amounts and tightening eligibility, often leaving creditworthy individuals underserved despite their repayment capacity. In contrast, credit scoring enhances accessibility by using quantitative data to assess risk more accurately, enabling lenders to extend credit to a broader range of applicants. This data-driven approach reduces information asymmetry and promotes fairer credit allocation, improving financial inclusion.

Technological Innovations Shaping Credit Evaluation

Technological innovations such as machine learning algorithms and big data analytics are revolutionizing credit evaluation by enhancing the accuracy and efficiency of credit scoring models. Unlike traditional credit rationing methods that rely on limited borrower information and manual assessments, advanced credit scoring harnesses real-time data from diverse sources, improving risk prediction and inclusivity. This transformation enables lenders to automate decision-making processes, reduce default rates, and expand credit access to underserved populations.

Future Trends: Integrating Rationing and Scoring in Credit Markets

Future trends in credit markets emphasize the integration of credit rationing and credit scoring to enhance lending precision and risk management. Advanced artificial intelligence algorithms analyze extensive borrower data to refine scoring models, while rationing mechanisms adjust credit availability based on real-time economic indicators and market conditions. This hybrid approach improves access to credit, reduces default rates, and supports more dynamic credit allocation strategies.

Important Terms

Adverse selection

Adverse selection occurs when lenders cannot differentiate between high-risk and low-risk borrowers, leading to credit rationing where some creditworthy applicants are denied loans to minimize risk exposure. Credit scoring systems mitigate adverse selection by using predictive algorithms and borrower data to accurately assess creditworthiness, thereby reducing the inefficiencies caused by credit rationing.

Soft information

Soft information, such as qualitative assessments of borrower character and local market knowledge, plays a crucial role in credit rationing by enabling lenders to make nuanced decisions beyond numerical data. Unlike credit scoring, which relies on quantitative metrics and algorithms, soft information captures contextual and relationship-based insights that improve credit access for borrowers with limited formal credit histories.

Hard information

Hard information, such as verified financial statements and credit scores, provides objective data that lenders use to assess borrower creditworthiness, enabling more precise credit scoring models. In contrast, credit rationing often occurs when lenders face limited hard information, leading to stricter lending criteria or denial of credit despite potentially creditworthy applicants.

Collateral requirements

Collateral requirements influence credit rationing by serving as a risk mitigation tool that lenders use when borrower creditworthiness is uncertain, often resulting in restricted loan amounts or higher rejection rates. In contrast, credit scoring relies on quantitative assessments of borrower data to streamline lending decisions, reducing the dependence on collateral and enabling broader access to credit.

Information asymmetry

Information asymmetry in credit markets leads lenders to rely on credit rationing when they cannot accurately assess borrower risk, limiting loan availability despite demand. Credit scoring reduces this asymmetry by providing quantifiable risk metrics, enabling more precise pricing and allocation of credit.

Relationship lending

Relationship lending leverages extensive borrower information and long-term interactions to reduce credit rationing by providing lenders with qualitative insights that credit scoring models, based primarily on quantitative data, may overlook. This personalized approach enhances credit access for small businesses and borrowers with limited credit history, as opposed to the standardized, algorithm-driven credit scoring which often results in stricter credit rationing due to its reliance on rigid criteria.

Underwriting models

Underwriting models leverage credit scoring algorithms to evaluate borrower risk and determine creditworthiness, enabling more precise credit rationing decisions by financial institutions. These models integrate quantitative credit scoring data with qualitative factors to optimize loan approval processes and mitigate default risk.

Loan pricing

Loan pricing is influenced by credit rationing, which limits loan availability despite borrowers' creditworthiness, while credit scoring enables lenders to assess risk more precisely and set interest rates accordingly. Integrating credit scoring reduces the need for rationing by allowing differentiated pricing based on individual credit profiles, enhancing market efficiency.

Financial inclusion

Financial inclusion expands access to credit for underserved populations by leveraging credit scoring models that use alternative data to reduce information asymmetry and mitigate credit rationing. Advanced credit scoring enhances risk assessment accuracy, enabling lenders to extend affordable credit to low-income borrowers traditionally excluded due to rigid credit rationing practices.

Automated decisioning

Automated decisioning leverages advanced algorithms and machine learning models to optimize credit rationing by evaluating credit risk more accurately than traditional credit scoring methods. This technology enhances financial institutions' ability to allocate credit efficiently, minimizing default rates and maximizing portfolio profitability through real-time data analysis and predictive modeling.

credit rationing vs credit scoring Infographic