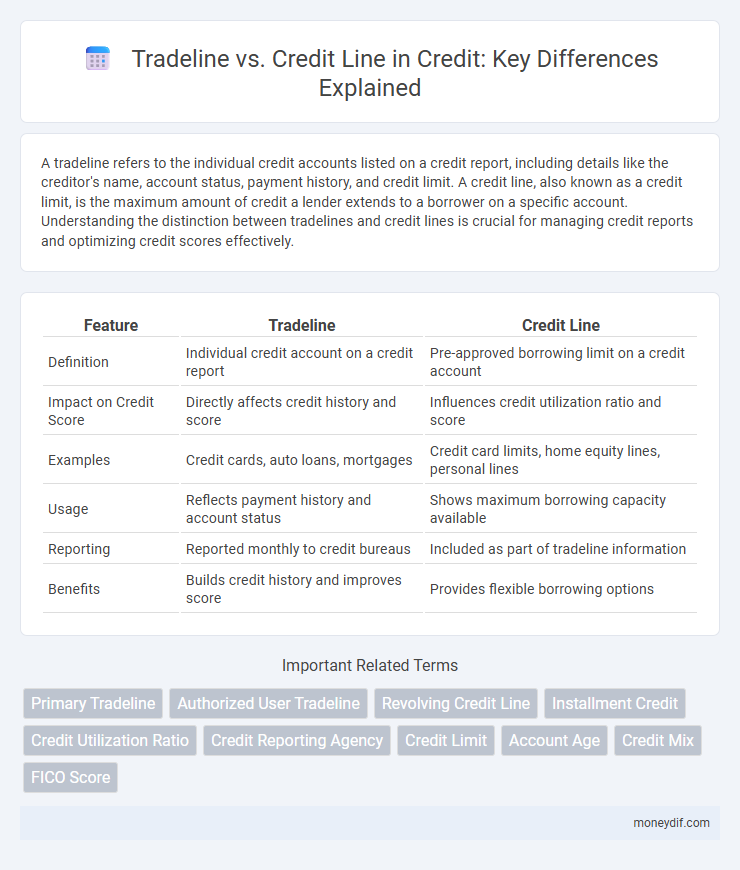

A tradeline refers to the individual credit accounts listed on a credit report, including details like the creditor's name, account status, payment history, and credit limit. A credit line, also known as a credit limit, is the maximum amount of credit a lender extends to a borrower on a specific account. Understanding the distinction between tradelines and credit lines is crucial for managing credit reports and optimizing credit scores effectively.

Table of Comparison

| Feature | Tradeline | Credit Line |

|---|---|---|

| Definition | Individual credit account on a credit report | Pre-approved borrowing limit on a credit account |

| Impact on Credit Score | Directly affects credit history and score | Influences credit utilization ratio and score |

| Examples | Credit cards, auto loans, mortgages | Credit card limits, home equity lines, personal lines |

| Usage | Reflects payment history and account status | Shows maximum borrowing capacity available |

| Reporting | Reported monthly to credit bureaus | Included as part of tradeline information |

| Benefits | Builds credit history and improves score | Provides flexible borrowing options |

Understanding Tradelines and Credit Lines

Tradelines are records of credit accounts on a consumer's credit report, detailing account type, balance, payment history, and credit limit, which impact credit score calculations. Credit lines refer to the maximum amount of credit a lender extends to a borrower on revolving accounts like credit cards or lines of credit. Understanding the differences between tradelines and credit lines helps in managing credit utilization and improving creditworthiness.

Key Differences Between Tradelines and Credit Lines

Tradelines represent the detailed records of credit accounts listed on a credit report, including payment history and account status. Credit lines refer to the maximum amount of credit extended by a lender that a borrower can use, such as credit card limits or revolving credit. Key differences lie in tradelines being documentation of credit activity, while credit lines indicate the available borrowing capacity tied to those accounts.

How Tradelines Impact Your Credit Report

Tradelines on your credit report detail each credit account you've opened, including payment history, credit limit, and account age, significantly influencing your credit score. Positive tradelines with consistent, on-time payments can boost your creditworthiness, while negative tradelines, such as late payments or defaults, can lower your credit score and impact loan eligibility. Understanding how tradelines affect your credit profile helps in managing credit health and optimizing borrowing potential.

Types of Credit Lines: Personal, Business, and More

Credit lines represent flexible borrowing options tailored to individual and business needs, including personal credit lines for everyday expenses and business credit lines designed for operational costs and growth. Types of credit lines vary broadly, encompassing secured lines backed by collateral, unsecured lines relying on creditworthiness, and specialized options like home equity lines of credit (HELOCs). Understanding these distinctions helps borrowers optimize financial strategies, improve cash flow management, and build a stronger credit profile.

Benefits of Adding Tradelines to Your Credit Profile

Adding tradelines to your credit profile can enhance your credit score by demonstrating a longer and more diverse credit history. Positive tradelines, such as authorized user accounts with strong payment records, improve credit utilization rates and payment history, which are key factors in credit scoring models like FICO and VantageScore. This strategy can lead to better loan terms, higher credit limits, and increased overall creditworthiness compared to solely relying on your existing credit lines.

Risks and Limitations of Buying Tradelines

Buying tradelines can artificially inflate credit scores but carries significant risks, including potential violations of credit reporting laws and the possibility of account closures by creditors. These practices may lead to fraudulent credit profiles, resulting in loan denials or legal consequences if discovered by lenders. Unlike a genuine credit line, purchased tradelines do not demonstrate real credit behavior, limiting their long-term impact on creditworthiness.

Credit Line Utilization and Credit Score Effects

Credit line utilization, calculated by dividing the outstanding balance by the total credit limit, significantly impacts credit scores by reflecting how much available credit is being used. Tradelines, which are individual credit accounts reported to credit bureaus, contribute to the overall credit utilization ratio when multiple credit lines are considered. Maintaining a low credit line utilization across tradelines generally enhances credit scores by demonstrating responsible credit management.

Tradeline Management vs. Credit Line Management

Tradeline management involves monitoring and optimizing individual credit accounts reported to credit bureaus, directly impacting credit scores by maintaining positive payment history and low utilization rates. Credit line management focuses on controlling the total available credit across all accounts, ensuring credit utilization stays within ideal levels to prevent score degradation and improve borrowing capacity. Effective tradeline management enhances credit profile accuracy, while credit line management strategically balances limits to support long-term credit health and financial flexibility.

Choosing Between Tradelines and Credit Lines for Credit Building

Choosing between tradelines and credit lines for credit building depends on individual financial goals and credit profiles. Tradelines reflect the detailed history of individual credit accounts reported to credit bureaus, directly impacting credit scores based on payment history, credit utilization, and account age. Credit lines, as revolving credit sources, provide flexible borrowing options and utilization management, influencing creditworthiness by maintaining low balances relative to credit limits.

Frequently Asked Questions: Tradeline vs. Credit Line

A tradeline is an individual credit account listed on a credit report, representing a borrower's history with a specific lender, while a credit line refers to the maximum amount of credit extended by a financial institution. Frequently asked questions often address how tradelines impact credit scores compared to overall credit lines and whether adding authorized user tradelines can improve credit health. Understanding the distinction helps consumers manage credit utilization, monitor credit report accuracy, and optimize their borrowing potential.

Important Terms

Primary Tradeline

Primary tradelines represent original credit accounts directly under a borrower's name, significantly impacting credit history and score. Unlike credit lines, which refer to the maximum available credit on an account, primary tradelines track actual payment history and balances, providing lenders with a clear view of credit behavior.

Authorized User Tradeline

An Authorized User Tradeline appears on a credit report when someone is added as an authorized user to another person's credit account, allowing the tradeline's history to influence their credit score without legal responsibility for the debt. Unlike a direct credit line, which the primary account holder controls and is personally liable for, an authorized user benefits from the credit line's payment history and credit utilization, potentially boosting credit profiles.

Revolving Credit Line

A revolving credit line allows borrowers to access funds up to a preset limit, with the balance replenishing as payments are made, unlike a tradeline which records specific credit accounts on a credit report but does not provide direct access to funds. Revolving credit lines impact credit utilization ratios, influencing credit scores more dynamically compared to static tradeline entries.

Installment Credit

Installment credit refers to loans with fixed monthly payments and a set repayment period, such as auto loans or mortgages, whereas a tradeline documents the activity and status of a credit account reported to credit bureaus, encompassing both installment and revolving credit lines. Understanding the distinction between a credit line, which is a revolving credit limit like a credit card, and an installment loan is essential for accurate credit reporting and scoring.

Credit Utilization Ratio

Credit Utilization Ratio measures the percentage of a credit line used through active tradelines, directly impacting credit scores by reflecting how much available credit is being utilized. Maintaining low utilization across individual tradelines helps optimize credit health and maximize overall credit potential.

Credit Reporting Agency

Credit reporting agencies collect and report data on tradelines, which represent individual credit accounts, highlighting payment history and credit utilization linked to specific credit lines such as credit cards or loans. Accurate tradeline information impacts credit scores by reflecting the status and limits of credit lines, influencing lending decisions and creditworthiness assessments.

Credit Limit

A credit limit refers to the maximum amount a lender allows a borrower to access on a credit line, while a tradeline is an entry on a credit report detailing credit-related activity, including credit limits, balances, and payment history. Credit lines define borrowing capacity, whereas tradelines provide a comprehensive record of credit utilization and repayment behaviors influencing credit scores.

Account Age

Account age significantly influences credit score calculations, with older tradelines typically contributing more positively due to a longer credit history. Tradelines represent individual credit accounts impacting overall credit utilization, while the credit line reflects the total credit limit available across all tradelines, making both factors crucial for assessing creditworthiness.

Credit Mix

Credit mix reflects the diversity of credit accounts on a credit report, including tradelines such as installment loans, credit cards, and revolving credit lines. Tradelines represent individual credit accounts, while credit lines specify the borrowing limits within those accounts, influencing credit utilization ratios and overall credit score impact.

FICO Score

FICO Score calculations prioritize the utilization ratio of individual tradelines over the total credit line available, meaning high balances on specific tradelines can lower the score even if overall credit usage is low. Each tradeline's credit limit and balance impact credit utilization rates, which directly influence FICO Scores by reflecting credit management efficiency.

Tradeline vs Credit line Infographic