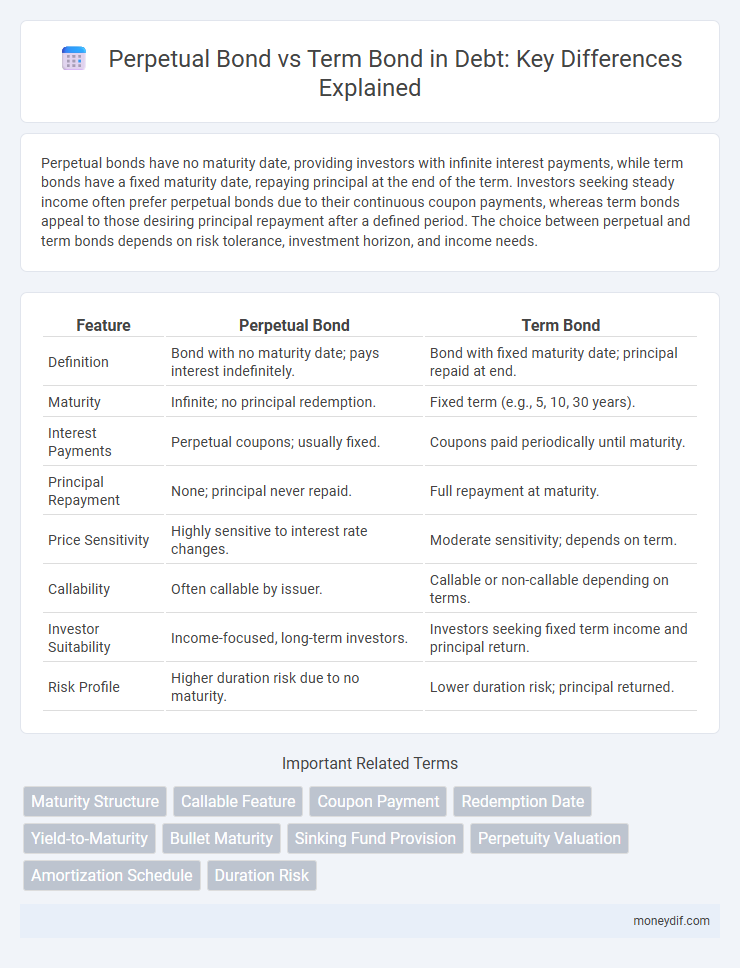

Perpetual bonds have no maturity date, providing investors with infinite interest payments, while term bonds have a fixed maturity date, repaying principal at the end of the term. Investors seeking steady income often prefer perpetual bonds due to their continuous coupon payments, whereas term bonds appeal to those desiring principal repayment after a defined period. The choice between perpetual and term bonds depends on risk tolerance, investment horizon, and income needs.

Table of Comparison

| Feature | Perpetual Bond | Term Bond |

|---|---|---|

| Definition | Bond with no maturity date; pays interest indefinitely. | Bond with fixed maturity date; principal repaid at end. |

| Maturity | Infinite; no principal redemption. | Fixed term (e.g., 5, 10, 30 years). |

| Interest Payments | Perpetual coupons; usually fixed. | Coupons paid periodically until maturity. |

| Principal Repayment | None; principal never repaid. | Full repayment at maturity. |

| Price Sensitivity | Highly sensitive to interest rate changes. | Moderate sensitivity; depends on term. |

| Callability | Often callable by issuer. | Callable or non-callable depending on terms. |

| Investor Suitability | Income-focused, long-term investors. | Investors seeking fixed term income and principal return. |

| Risk Profile | Higher duration risk due to no maturity. | Lower duration risk; principal returned. |

Understanding Perpetual Bonds: Definition and Features

Perpetual bonds, also known as consols, are fixed-income securities with no maturity date, paying interest indefinitely, unlike term bonds which have a specified maturity period. These bonds provide issuers with long-term capital without repayment obligations, but they expose investors to interest rate risk and potential price volatility. Key features include fixed coupon payments, lack of principal repayment, and sensitivity to market interest rate fluctuations, making them suitable for investors seeking steady income streams over an extended period.

What Are Term Bonds? Key Characteristics

Term bonds are debt securities with a fixed maturity date, requiring the issuer to repay the principal amount in full at the end of the term. They often pay periodic interest, known as coupon payments, throughout the bond's life. Key characteristics include a defined maturity period, interest rate stability, and predictable cash flow for investors compared to perpetual bonds, which have no maturity date.

Interest Payment Structure: Perpetual vs Term Bonds

Perpetual bonds pay interest indefinitely without a fixed maturity date, providing continuous coupon payments to investors. Term bonds have a set maturity date, requiring interest payments only until repayment of principal at maturity. This difference influences cash flow predictability and risk profiles for holders of perpetual versus term bonds.

Maturity and Redemption: A Core Difference

Perpetual bonds lack a fixed maturity date, providing interest payments indefinitely without a scheduled redemption, whereas term bonds have a predetermined maturity date at which the principal is repaid. This fundamental difference affects cash flow predictability and investor risk profiles, with perpetual bonds exhibiting higher interest rate sensitivity. Issuers favor term bonds for defined capital repayment timelines, while perpetual bonds serve as a hybrid of debt and equity on balance sheets.

Risk Profiles: Assessing Default and Interest Rate Risks

Perpetual bonds carry higher interest rate risk due to their indefinite duration, making their prices more sensitive to market rate fluctuations compared to term bonds with fixed maturity dates. Term bonds, while exposed to default risk over a defined time frame, offer clearer timelines for repayment, reducing uncertainty for investors. Investors must weigh the perpetual bond's potential for steady income against the increased risk of principal fluctuation and the term bond's relative stability in income but finite risk exposure.

Yield Comparison: How Do Returns Differ?

Perpetual bonds offer a fixed interest payment indefinitely, typically resulting in lower yields compared to term bonds due to their infinite maturity risk. Term bonds provide a defined maturity date, allowing investors to realize principal repayment and usually offer higher yields to compensate for time-bound credit risk. Yield differences arise from the trade-off between perpetual income streams and the finite risk exposure associated with term bonds.

Liquidity and Market Demand Factors

Perpetual bonds typically exhibit lower liquidity compared to term bonds due to their indefinite maturity, which can deter short-term investors seeking predictable redemption dates. Market demand often favors term bonds as they offer clearer cash flow timelines and risk profiles, aligning with institutional investors' portfolio strategies. The fixed maturity of term bonds enhances marketability, contributing to higher trading volumes and tighter bid-ask spreads relative to perpetual bonds.

Suitability for Investors: Matching Goals with Bond Types

Perpetual bonds, offering indefinite interest payments without principal repayment, suit investors seeking steady income and long-term holding horizons. Term bonds, with fixed maturity dates and principal repayment, appeal to investors prioritizing capital preservation and predictable cash flows. Choosing between these bond types depends on aligning investor risk tolerance, income needs, and investment timelines to optimize portfolio objectives.

How Perpetual and Term Bonds Affect Issuers

Perpetual bonds provide issuers with indefinite borrowing without principal repayment, reducing refinancing risk but potentially increasing long-term interest expenses due to perpetual coupon payments. Term bonds require issuers to repay the principal at maturity, creating a defined debt timeline and necessitating future refinancing or repayment strategies that may impact liquidity. Issuers must balance the perpetual bond's continuous cost against the term bond's maturity risk to optimize capital structure and manage cash flows effectively.

Perpetual vs Term Bonds: Which Fits Your Portfolio?

Perpetual bonds offer unlimited interest payments without a maturity date, providing steady income but limited capital return, making them suitable for income-focused portfolios. Term bonds have fixed maturities, offering predictable principal repayment alongside interest, appealing to investors seeking capital preservation and defined investment horizons. Portfolio fit depends on risk tolerance, cash flow needs, and investment timeline.

Important Terms

Maturity Structure

Maturity structure impacts investment strategy as perpetual bonds have no fixed maturity date, providing indefinite interest payments, whereas term bonds have a specified maturity date, returning principal at the end of the term.

Callable Feature

Callable features in perpetual bonds allow issuers to redeem the bonds before maturity, providing flexibility compared to term bonds that have fixed maturity dates without early redemption options.

Coupon Payment

Coupon payments on perpetual bonds are fixed interest payments made indefinitely without a maturity date, providing investors with a steady income stream, whereas term bonds offer coupon payments only until the bond's maturity, after which the principal is repaid. The value of coupon payments in perpetual bonds depends on the prevailing interest rates, while term bonds combine coupon payments and principal repayment, impacting their overall yield and price sensitivity.

Redemption Date

Redemption date for perpetual bonds is indefinite with no maturity, unlike term bonds which have a fixed redemption date when principal is repaid.

Yield-to-Maturity

Yield-to-Maturity (YTM) on perpetual bonds is calculated based on infinite coupon payments without principal redemption, resulting in YTM equating the annual coupon divided by the current price, while term bonds have a finite maturity where YTM incorporates both coupon payments and the return of face value at maturity. This fundamental difference means YTM for perpetual bonds reflects ongoing income yield, whereas term bond YTM captures total return over a specified period, impacting investment valuation and duration assessment.

Bullet Maturity

Bullet maturity refers to a bond structure where the principal amount is repaid in a single lump sum at the end of the term, commonly seen in term bonds rather than perpetual bonds. Perpetual bonds lack a fixed maturity date and only pay interest indefinitely, while term bonds with bullet maturity repay the entire principal upon maturity, offering clear redemption timing for investors.

Sinking Fund Provision

The sinking fund provision in a bond requires the issuer to set aside funds regularly to repay part of the bond principal before maturity, which is more common in term bonds than perpetual bonds due to the defined maturity date of term bonds. Perpetual bonds typically lack a sinking fund because their interest payments continue indefinitely without a principal repayment schedule, making the sinking fund unnecessary or impractical.

Perpetuity Valuation

Perpetuity valuation involves calculating the present value of infinite cash flows, a method commonly applied to perpetual bonds that pay fixed coupons indefinitely without maturity. In contrast, term bonds have a defined maturity date, requiring valuation models to consider both the finite series of coupon payments and the principal repayment at the end of the term.

Amortization Schedule

An amortization schedule for a term bond outlines the periodic principal and interest payments until maturity, enabling investors to track the gradual reduction of debt, whereas a perpetual bond lacks a maturity date and does not have an amortization schedule since principal repayment is never required. Term bonds provide defined cash flow timelines through amortization, while perpetual bonds offer indefinite interest payments without principal amortization, affecting investment valuation and cash flow projections.

Duration Risk

Duration risk is higher in perpetual bonds than term bonds due to their indefinite maturity causing greater sensitivity to interest rate changes.

perpetual bond vs term bond Infographic