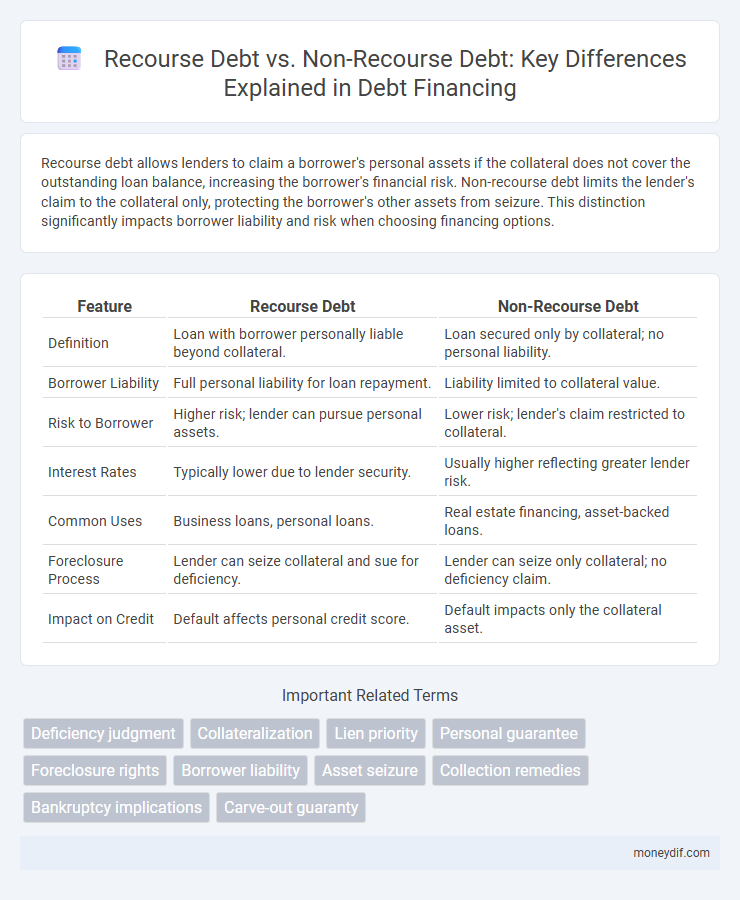

Recourse debt allows lenders to claim a borrower's personal assets if the collateral does not cover the outstanding loan balance, increasing the borrower's financial risk. Non-recourse debt limits the lender's claim to the collateral only, protecting the borrower's other assets from seizure. This distinction significantly impacts borrower liability and risk when choosing financing options.

Table of Comparison

| Feature | Recourse Debt | Non-Recourse Debt |

|---|---|---|

| Definition | Loan with borrower personally liable beyond collateral. | Loan secured only by collateral; no personal liability. |

| Borrower Liability | Full personal liability for loan repayment. | Liability limited to collateral value. |

| Risk to Borrower | Higher risk; lender can pursue personal assets. | Lower risk; lender's claim restricted to collateral. |

| Interest Rates | Typically lower due to lender security. | Usually higher reflecting greater lender risk. |

| Common Uses | Business loans, personal loans. | Real estate financing, asset-backed loans. |

| Foreclosure Process | Lender can seize collateral and sue for deficiency. | Lender can seize only collateral; no deficiency claim. |

| Impact on Credit | Default affects personal credit score. | Default impacts only the collateral asset. |

Understanding Recourse Debt and Non-Recourse Debt

Recourse debt allows lenders to claim the borrower's personal assets if the collateral does not cover the outstanding loan balance, thereby increasing the borrower's financial risk. Non-recourse debt limits the lender's recovery strictly to the collateral securing the loan, protecting the borrower's other assets from liability. Understanding the distinctions between recourse debt and non-recourse debt is essential for managing financial risk in real estate, business loans, and personal financing.

Key Differences Between Recourse and Non-Recourse Debt

Recourse debt allows lenders to pursue the borrower's other assets beyond the collateral in case of default, increasing the borrower's risk exposure. Non-recourse debt limits lender recovery solely to the collateral securing the loan, protecting the borrower's additional assets. This fundamental difference affects loan terms, interest rates, and borrower liability.

Legal Implications of Recourse Debt

Recourse debt legally allows lenders to pursue the borrower's personal assets beyond the collateral if the loan defaults, increasing the borrower's financial risk. This legal obligation means borrowers remain fully liable for repayment, potentially resulting in wage garnishment or asset seizure. In contrast, non-recourse debt limits lender recovery solely to the collateral, protecting personal assets from creditor claims.

Legal Protections Under Non-Recourse Debt

Non-recourse debt offers substantial legal protections by limiting the lender's recovery exclusively to the collateral specified in the loan agreement, preventing personal liability for the borrower beyond the asset securing the loan. This means that if the borrower defaults, the lender can seize the collateral but cannot pursue the borrower's other assets or income. Such protections are particularly significant in real estate financing, where non-recourse loans reduce the borrower's risk exposure while encouraging investment in high-value properties.

Impact on Borrowers and Lenders

Recourse debt allows lenders to pursue a borrower's other assets if the collateral does not cover the outstanding loan balance, increasing the borrower's financial risk and incentivizing careful repayment. Non-recourse debt limits the lender's recovery to the collateral alone, reducing borrower liability but increasing lender risk, often resulting in higher interest rates or stricter loan terms. This dynamic affects loan structuring, asset protection strategies, and risk management for both parties in debt agreements.

Risk Assessment: Recourse vs Non-Recourse Loans

Recourse debt exposes borrowers to personal liability, allowing lenders to pursue assets beyond the collateral if the loan defaults, increasing overall financial risk. Non-recourse debt limits the lender's claim strictly to the collateral, reducing borrower risk but often resulting in higher interest rates or stricter lending criteria. Risk assessment for these loan types requires evaluating borrower creditworthiness, asset value, and potential recovery scenarios to balance lender protection against borrower exposure.

Common Examples of Recourse Debt

Common examples of recourse debt include credit card balances, personal loans, and most types of auto loans, where the borrower is personally liable beyond the collateral. Mortgages are often recourse loans depending on state laws, meaning lenders can pursue the borrower's other assets if the property value doesn't cover the outstanding debt. Business loans with personal guarantees also qualify as recourse debt, exposing owners to personal liability in case of default.

Common Examples of Non-Recourse Debt

Common examples of non-recourse debt include mortgage loans secured by residential and commercial real estate, where the lender's recovery is limited to the collateral's value. Auto loans in certain jurisdictions may also be structured as non-recourse, protecting borrowers from personal liability beyond the vehicle itself. Additionally, project finance loans often utilize non-recourse structures, restricting lender claims to project assets and revenue streams exclusively.

Factors to Consider When Choosing Between Recourse and Non-Recourse Debt

Evaluating factors such as risk tolerance, asset protection, and loan terms is crucial when choosing between recourse and non-recourse debt. Recourse debt typically offers lower interest rates but exposes borrowers to personal liability beyond the collateral, while non-recourse debt limits liability to the collateral but often comes with higher interest rates and stricter approval criteria. Understanding these trade-offs helps borrowers align financing options with their financial goals and risk management strategies.

Recourse Debt vs Non-Recourse Debt: Which Is Right for You?

Recourse debt holds borrowers personally liable, allowing lenders to pursue assets beyond the collateral if the loan defaults, providing greater security for lenders but higher risk for borrowers. Non-recourse debt limits lenders' claims strictly to the collateral, protecting borrowers' other assets but often resulting in higher interest rates or stricter credit requirements. Choosing between recourse and non-recourse debt depends on risk tolerance, loan purpose, and financial stability, making it essential to evaluate personal liability exposure and asset protection carefully.

Important Terms

Deficiency judgment

Deficiency judgment occurs when a borrower's recourse debt balance exceeds the foreclosure sale price, allowing lenders to pursue the borrower personally, whereas non-recourse debt limits lender recovery solely to the collateral property, preventing personal liability.

Collateralization

Collateralization in recourse debt allows lenders to claim assets beyond the collateral, whereas non-recourse debt restricts lender claims solely to the secured collateral.

Lien priority

Lien priority determines the order in which creditors are paid from the collateral's sale, with recourse debt allowing lenders to pursue the borrower's other assets beyond the lien, while non-recourse debt limits the lender's recovery to the collateral only. In cases of default, recourse debt typically holds a stronger position due to the lender's ability to seek additional repayment, whereas non-recourse debt is secured solely by the property tied to the lien's priority.

Personal guarantee

A personal guarantee in recourse debt holds the borrower personally liable, allowing the lender to pursue the borrower's assets beyond collateral if the loan defaults, whereas non-recourse debt limits the lender's recovery solely to the secured collateral without personal liability. Understanding the distinction between recourse and non-recourse debt is critical for assessing financial risk and legal obligations in loan agreements involving personal guarantees.

Foreclosure rights

Foreclosure rights differ significantly between recourse debt, where lenders can pursue borrowers for remaining balances after foreclosure, and non-recourse debt, where lenders can only seize the collateral property without claiming additional repayment.

Borrower liability

Borrower liability in recourse debt holds the borrower personally responsible for repayment beyond collateral value, whereas non-recourse debt limits liability solely to the collateral securing the loan.

Asset seizure

Asset seizure typically occurs in recourse debt agreements where lenders can claim borrower assets upon default, whereas in non-recourse debt, lenders have limited rights and can only seize collateral specifically tied to the loan without pursuing further borrower assets. The legal framework surrounding recourse debt increases borrower risk by extending creditor claims beyond the secured asset, while non-recourse loans limit lender recovery to the collateral, protecting the borrower's other assets.

Collection remedies

Collection remedies for recourse debt allow lenders to pursue the borrower's other assets beyond collateral, while non-recourse debt limits recovery strictly to the collateral securing the loan.

Bankruptcy implications

Bankruptcy implications differ significantly between recourse and non-recourse debt, as recourse debt allows lenders to pursue the borrower's other assets beyond the collateral, increasing personal liability risk. Non-recourse debt limits lender claims strictly to the collateral, protecting the borrower's personal assets even if the collateral's value falls short during bankruptcy proceedings.

Carve-out guaranty

A carve-out guaranty limits the guarantor's liability to specified recourse debt obligations, excluding non-recourse debt from personal guarantee claims.

recourse debt vs non-recourse debt Infographic