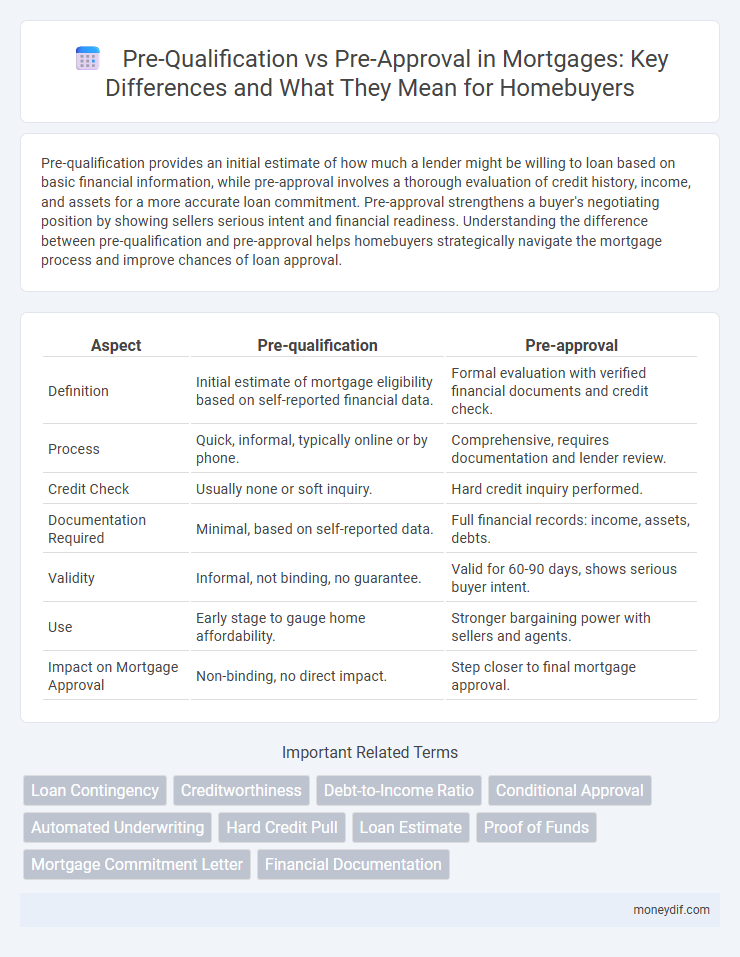

Pre-qualification provides an initial estimate of how much a lender might be willing to loan based on basic financial information, while pre-approval involves a thorough evaluation of credit history, income, and assets for a more accurate loan commitment. Pre-approval strengthens a buyer's negotiating position by showing sellers serious intent and financial readiness. Understanding the difference between pre-qualification and pre-approval helps homebuyers strategically navigate the mortgage process and improve chances of loan approval.

Table of Comparison

| Aspect | Pre-qualification | Pre-approval |

|---|---|---|

| Definition | Initial estimate of mortgage eligibility based on self-reported financial data. | Formal evaluation with verified financial documents and credit check. |

| Process | Quick, informal, typically online or by phone. | Comprehensive, requires documentation and lender review. |

| Credit Check | Usually none or soft inquiry. | Hard credit inquiry performed. |

| Documentation Required | Minimal, based on self-reported data. | Full financial records: income, assets, debts. |

| Validity | Informal, not binding, no guarantee. | Valid for 60-90 days, shows serious buyer intent. |

| Use | Early stage to gauge home affordability. | Stronger bargaining power with sellers and agents. |

| Impact on Mortgage Approval | Non-binding, no direct impact. | Step closer to final mortgage approval. |

Understanding Pre-Qualification in Mortgages

Pre-qualification in mortgages is an initial assessment where lenders evaluate a borrower's financial information, such as income, assets, and debts, to estimate the loan amount they might qualify for. This process is usually quick and informal, often requiring only self-reported data without rigorous verification, providing prospective buyers a general idea of their purchasing power. Understanding pre-qualification helps borrowers gauge affordability and guides them in starting the home search before pursuing the more detailed and binding pre-approval process.

What is Mortgage Pre-Approval?

Mortgage pre-approval is a formal process where a lender evaluates a borrower's financial background--including credit score, income, and debt--to determine the maximum loan amount they qualify for. This involves submitting documentation such as pay stubs, tax returns, and credit reports, resulting in a conditional commitment indicating the lender's willingness to fund the mortgage. Pre-approval strengthens a buyer's position in the homebuying market by demonstrating serious intent to sellers and real estate agents.

Key Differences Between Pre-Qualification and Pre-Approval

Pre-qualification for a mortgage provides an initial estimate of how much a borrower might afford based on self-reported financial information without in-depth verification. Pre-approval involves a thorough evaluation of credit history, income, assets, and debts by a lender, resulting in a conditional commitment to lend a specific amount. Key differences include the level of documentation required, the lender's commitment strength, and the impact on the borrower's bargaining power during home buying.

Benefits of Getting Pre-Qualified

Getting pre-qualified for a mortgage provides a clear estimate of the loan amount you may qualify for, helping you set a realistic budget when house hunting. It requires minimal documentation, making it a quick and convenient way to gauge your financial standing with lenders. This preliminary step boosts your confidence and allows for smoother negotiations with sellers by demonstrating your seriousness as a buyer.

Advantages of Mortgage Pre-Approval

Mortgage pre-approval offers significant advantages by providing a clear estimate of the loan amount you qualify for, enhancing your bargaining power with sellers. It streamlines the homebuying process by expediting loan approval and reducing uncertainties, making your offer more credible. Lenders verify your financial background during pre-approval, minimizing the risk of last-minute surprises and improving your chances of closing the deal quickly.

How Lenders Evaluate Pre-Qualification vs Pre-Approval

Lenders evaluate pre-qualification based primarily on self-reported financial information, offering a preliminary estimate of borrowing capacity without rigorous verification. Pre-approval involves thorough scrutiny of credit reports, income documentation, and assets, providing a conditional commitment on loan amount. This detailed assessment in pre-approval enhances buyer credibility and streamlines the mortgage approval process.

Required Documents for Pre-Qualification and Pre-Approval

Pre-qualification for a mortgage typically requires basic information such as income, assets, debts, and credit score, often provided verbally or through a simple form, without the need for detailed documentation. Pre-approval demands comprehensive documentation, including recent pay stubs, tax returns, bank statements, employment verification, and authorization for a credit check, ensuring a thorough assessment of the borrower's financial status. The pre-approval process offers a more accurate estimate of loan eligibility and demonstrates stronger buyer credibility to sellers.

Which Comes First: Pre-Qualification or Pre-Approval?

Pre-qualification typically comes first in the mortgage process, offering a preliminary estimate of how much a borrower might qualify for based on self-reported financial information. Pre-approval follows, involving a thorough review of the borrower's credit, income, and assets by the lender, resulting in a conditional commitment for a specific loan amount. Understanding the sequence helps borrowers strengthen their position before shopping for homes and submitting offers.

Impact on Home Shopping and Negotiation Power

Pre-approval provides a stronger negotiation position and greater confidence during home shopping by verifying creditworthiness and loan eligibility with a lender, unlike pre-qualification which is an initial estimate based on self-reported information. Buyers with pre-approval letters are often prioritized by sellers and real estate agents because their financing is more certain, streamlining the purchase process. Pre-qualification serves as a preliminary step but does not guarantee loan approval, limiting its impact on competitive bidding and offer strength.

Choosing the Best Option for Your Home Buying Journey

Pre-qualification offers a quick estimate of your borrowing potential based on self-reported financial information, ideal for early-stage homebuyers exploring options without commitment. Pre-approval involves a thorough verification of your credit, income, and assets by a lender, providing a conditional loan offer that strengthens your position when making an offer on a property. Choosing between pre-qualification and pre-approval depends on your readiness to proceed, with pre-approval generally preferred for serious buyers aiming to expedite the closing process and enhance negotiating power.

Important Terms

Loan Contingency

Loan contingency protects buyers by allowing contract cancellation if financing falls through, relying on either pre-qualification or pre-approval status; pre-approval provides stronger assurance to sellers as it involves a thorough credit check and verified financial documents, whereas pre-qualification is a preliminary estimate based on self-reported information. Real estate transactions benefit from loan contingencies tied to pre-approval because they reduce uncertainty and increase buyer credibility.

Creditworthiness

Creditworthiness assessment plays a critical role in distinguishing pre-qualification from pre-approval, as pre-qualification offers an initial estimate based on self-reported financial information while pre-approval includes a thorough examination of credit reports, income, and debt, providing a more accurate and reliable indication of loan eligibility. Lenders use detailed creditworthiness data during pre-approval to lock interest rates and loan terms, making it a stronger position for buyers in competitive real estate markets.

Debt-to-Income Ratio

Debt-to-Income Ratio (DTI) plays a crucial role in both pre-qualification and pre-approval processes, with lenders assessing this ratio to determine a borrower's ability to manage monthly payments relative to income. Pre-approval typically requires a more detailed and accurate DTI calculation, as it involves verification of income, debts, and credit, whereas pre-qualification often relies on self-reported financial information and provides an initial estimate.

Conditional Approval

Conditional approval is a mortgage status granted after pre-qualification and pre-approval stages, indicating the lender's tentative agreement based on initial document review but subject to further verification. Unlike pre-qualification, which is a basic credit assessment, and pre-approval, which involves a more comprehensive underwriting process, conditional approval requires borrowers to fulfill specified conditions such as updated income verification or property appraisal before final loan commitment.

Automated Underwriting

Automated underwriting uses algorithms to analyze credit risk swiftly, enabling real-time decisions during the pre-qualification process, which typically offers borrowers an estimate of their loan eligibility based on minimal financial data. Pre-approval, involving a more thorough automated underwriting review, verifies detailed financial documents and credit history, providing a conditional commitment that strengthens the borrower's position in the home buying process.

Hard Credit Pull

A hard credit pull occurs during the pre-approval process, where lenders thoroughly assess an applicant's full credit report to determine loan eligibility, which can slightly impact credit scores. In contrast, pre-qualification typically involves a soft credit inquiry that estimates borrowing potential without affecting credit ratings or committing the lender to approve the loan.

Loan Estimate

Loan Estimate provides a detailed breakdown of estimated loan terms and costs after pre-approval, offering a more accurate financial picture than pre-qualification, which is a preliminary assessment based on basic financial information. Pre-approval involves a thorough credit check and documentation review, making the Loan Estimate a crucial tool for comparing loan offers and understanding true borrowing costs.

Proof of Funds

Proof of Funds demonstrates a buyer's financial capability by verifying available liquid assets, crucial during property negotiations and making offers. Pre-qualification provides an initial estimate of borrowing capacity based on self-reported financial information, while pre-approval involves thorough lender verification of income, credit, and assets, offering stronger assurance to sellers.

Mortgage Commitment Letter

A Mortgage Commitment Letter represents a lender's formal promise to fund a loan pending specific conditions, providing stronger assurance than pre-qualification or pre-approval stages. While pre-qualification offers a preliminary estimate of borrowing potential and pre-approval involves a more detailed financial review, the commitment letter confirms loan approval subject to verification of final documentation.

Financial Documentation

Financial documentation for pre-qualification typically includes basic income statements, credit score reports, and employment verification, offering a preliminary assessment of a borrower's ability to qualify for a loan. Pre-approval requires comprehensive financial documents such as tax returns, bank statements, and debt-to-income ratios, providing a more definitive commitment based on thorough evaluation by lenders.

Pre-qualification vs Pre-approval Infographic