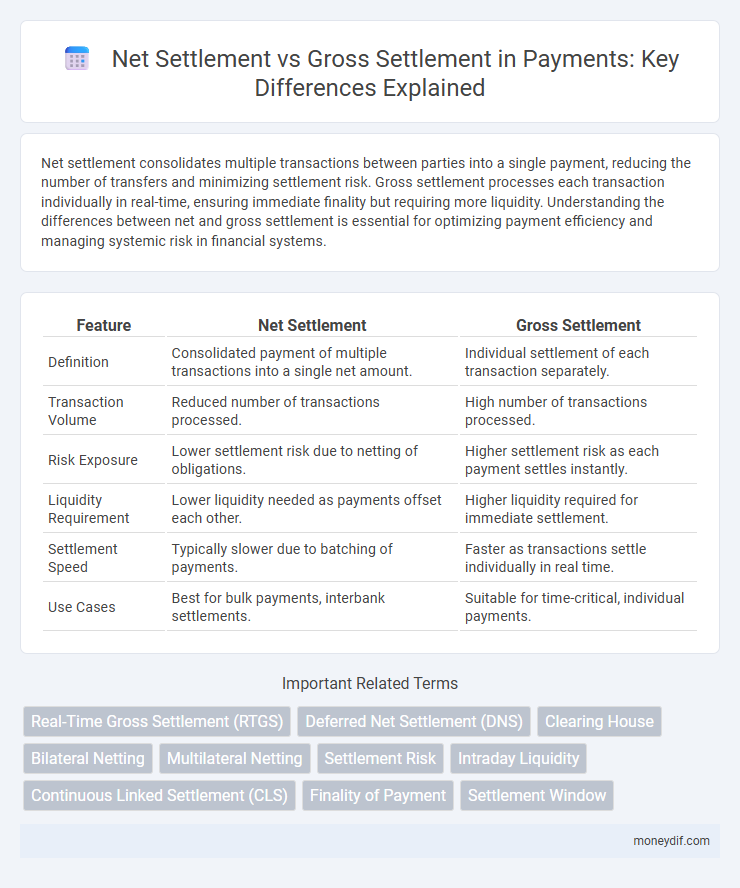

Net settlement consolidates multiple transactions between parties into a single payment, reducing the number of transfers and minimizing settlement risk. Gross settlement processes each transaction individually in real-time, ensuring immediate finality but requiring more liquidity. Understanding the differences between net and gross settlement is essential for optimizing payment efficiency and managing systemic risk in financial systems.

Table of Comparison

| Feature | Net Settlement | Gross Settlement |

|---|---|---|

| Definition | Consolidated payment of multiple transactions into a single net amount. | Individual settlement of each transaction separately. |

| Transaction Volume | Reduced number of transactions processed. | High number of transactions processed. |

| Risk Exposure | Lower settlement risk due to netting of obligations. | Higher settlement risk as each payment settles instantly. |

| Liquidity Requirement | Lower liquidity needed as payments offset each other. | Higher liquidity required for immediate settlement. |

| Settlement Speed | Typically slower due to batching of payments. | Faster as transactions settle individually in real time. |

| Use Cases | Best for bulk payments, interbank settlements. | Suitable for time-critical, individual payments. |

Introduction to Payment Settlements

Net settlement aggregates multiple payment transactions into a single net amount to be transferred between parties, reducing transaction volumes and enhancing liquidity management. Gross settlement processes each payment instruction individually and immediately, ensuring finality and minimizing credit risk. Understanding the distinctions between net and gross settlement is crucial for financial institutions to optimize payment efficiency and mitigate systemic risks.

Understanding Net Settlement

Net settlement consolidates multiple payment obligations between parties into a single, final payment, reducing the number of transactions and liquidity requirements. This method contrasts with gross settlement, where each transaction is settled individually in real time. Understanding net settlement is crucial for managing counterparty risk and improving operational efficiency in payment systems.

Overview of Gross Settlement

Gross settlement processes each transaction individually and immediately, ensuring the full payment amount is transferred without netting against other transactions. This method enhances payment finality and reduces counterparty risk by settling transactions in real-time or near real-time. Gross settlement systems are commonly used in high-value payment infrastructures such as Real-Time Gross Settlement (RTGS) systems operated by central banks.

Key Differences Between Net and Gross Settlement

Net settlement processes aggregate multiple payment obligations to settle the final net amount between parties, reducing transaction volume and liquidity requirements. Gross settlement involves the immediate, individual payment of each transaction, offering real-time finality and minimizing credit risk but requiring higher liquidity. Key differences include liquidity usage, timing of settlement, and risk exposure, with net settlement optimized for efficiency and gross settlement prioritized for speed and security.

Efficiency and Cost Implications

Net settlement consolidates multiple payment obligations into a single transaction, significantly enhancing efficiency by reducing the number of transfers and minimizing liquidity requirements. Gross settlement processes each payment individually in real time, increasing operational costs and requiring higher liquidity to cover each transaction immediately. Financial institutions often prefer net settlement to optimize cash flows and lower transaction expenses, while gross settlement is favored in high-value, time-sensitive payments despite its higher cost implications.

Risk Management in Settlement Systems

Net settlement reduces credit and liquidity risk by aggregating multiple transactions into a single net payment, minimizing the amount of funds transferred between parties. Gross settlement processes each transaction individually in real time, eliminating settlement risk but requiring greater liquidity and operational capacity. Payment systems balance these approaches to optimize risk management, with net settlement systems often relying on collateral and guarantees to mitigate timing risk.

Speed of Funds Transfer

Net settlement consolidates multiple transactions into a single sum, significantly enhancing the speed of funds transfer by reducing processing time and operational load on payment systems. Gross settlement processes each transaction individually, ensuring real-time transfer but often causing delays due to higher liquidity requirements and increased settlement risk management. Faster speed of funds transfer in net settlement benefits institutions by minimizing clearing cycles, while gross settlement provides immediate finality essential for high-value payments.

Regulatory and Compliance Considerations

Net settlement reduces systemic risk by consolidating multiple transactions into a single payment, aligning with regulatory frameworks like the European Central Bank's TARGET2 for efficient liquidity management. Gross settlement requires immediate, individual transaction processing, ensuring real-time finality and compliance with anti-money laundering (AML) and know-your-customer (KYC) regulations. Regulatory authorities emphasize transparency and risk mitigation, mandating robust reporting standards and operational oversight for both net and gross settlement systems.

Use Cases and Industry Applications

Net settlement is commonly used in retail banking and card payment networks where multiple transactions are aggregated to reduce liquidity requirements and operational costs. Gross settlement is preferred in high-value or time-critical transfers such as interbank payments and real-time gross settlement systems (RTGS), ensuring immediate finality and reducing settlement risk. Payment processors, financial institutions, and clearinghouses apply these methods according to transaction volume, risk tolerance, and settlement speed demands.

Choosing the Right Settlement Method

Choosing the right settlement method depends on transaction volume and risk tolerance, where net settlement aggregates multiple transactions for a single payment, reducing liquidity needs and operational costs. Gross settlement processes each transaction individually, offering immediate finality and minimized credit risk, often preferred in high-value or time-sensitive transactions. Financial institutions must balance efficiency against risk exposure to optimize cash flow and security in payment processing.

Important Terms

Real-Time Gross Settlement (RTGS)

Real-Time Gross Settlement (RTGS) systems process high-value interbank payments individually and immediately, ensuring finality without netting debits and credits. Unlike net settlement systems that batch transactions and settle the net amount at intervals, RTGS minimizes settlement risk by settling each transaction on a gross basis in real time.

Deferred Net Settlement (DNS)

Deferred Net Settlement (DNS) aggregates multiple payment obligations over a specific period before calculating a single net payment amount, enhancing liquidity efficiency compared to Gross Settlement systems that settle each transaction individually and immediately. DNS reduces the total number of settlements by offsetting debits and credits, lowering transaction costs and risk exposure in high-volume financial networks.

Clearing House

Clearing houses facilitate net settlement by aggregating multiple transactions between parties into a single net amount, reducing the total funds and securities exchanged, while gross settlement involves the immediate, individual settlement of each transaction in real time. Net settlement enhances liquidity efficiency and lowers counterparty risk, whereas gross settlement prioritizes finality and reduces settlement risk by processing payments individually and continuously throughout the day.

Bilateral Netting

Bilateral netting consolidates multiple transactions between two parties into a single net payment, reducing settlement risk and liquidity needs compared to gross settlement, where each transaction is settled individually. This method enhances operational efficiency and lowers counterparty exposure by minimizing the total value of payments exchanged daily.

Multilateral Netting

Multilateral netting consolidates multiple payment obligations among several parties into a single net payment, significantly reducing the total transaction volume compared to gross settlement, where each payment is settled individually and in full. This process enhances liquidity efficiency and minimizes systemic risk by lowering the amount of funds that must be exchanged across the network at settlement time.

Settlement Risk

Settlement risk arises when transactions are processed through net settlement systems, as obligations are aggregated and settled at specific intervals, increasing exposure to counterparty default before final settlement. In contrast, gross settlement systems mitigate settlement risk by processing each transaction individually and immediately, ensuring real-time finality and reducing the likelihood of default contagion.

Intraday Liquidity

Intraday liquidity management is critical for facilitating smooth net settlement processes, where only the net difference between payments is transferred, reducing the need for large liquidity buffers compared to gross settlement systems that require full payment amounts to be available throughout the day. Efficient intraday liquidity allocation enhances payment system stability by minimizing settlement risks and optimizing the use of central bank reserves in both net and gross settlement frameworks.

Continuous Linked Settlement (CLS)

Continuous Linked Settlement (CLS) significantly reduces settlement risk in foreign exchange transactions by employing a payment-versus-payment (PvP) mechanism that ensures simultaneous settlement of both legs of a trade. Unlike gross settlement, where each transaction is settled individually, CLS uses a net settlement process across multiple currencies, optimizing liquidity and minimizing the risk of settlement failures.

Finality of Payment

Finality of payment ensures that a transaction is irrevocably completed and legally binding, which is critical in both net settlement and gross settlement systems. Net settlement aggregates multiple payments into a single net amount to reduce liquidity needs but introduces settlement risk until finality is achieved, whereas gross settlement processes each payment individually and finalizes transactions immediately, minimizing credit risk.

Settlement Window

The settlement window determines the timeframe within which financial transactions must be finalized in net settlement systems, enabling aggregation of multiple obligations to reduce the number of payments and liquidity needs compared to gross settlement, where each transaction is settled individually in real-time. Efficient management of the settlement window in net settlement systems mitigates counterparty risk and enhances overall system liquidity by optimizing the timing of payment netting and fund transfers.

net settlement vs gross settlement Infographic