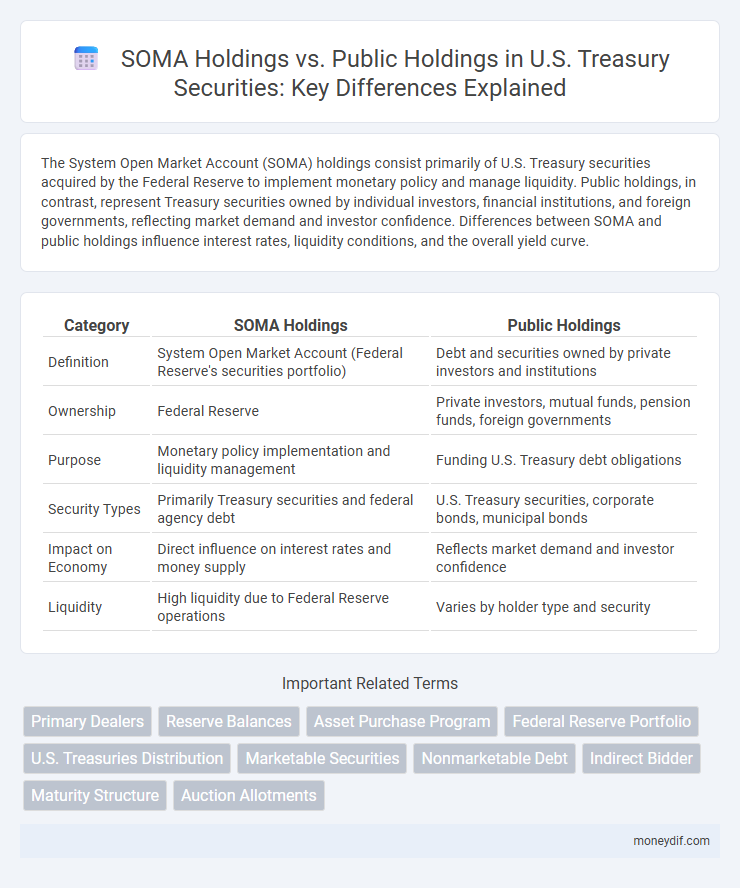

The System Open Market Account (SOMA) holdings consist primarily of U.S. Treasury securities acquired by the Federal Reserve to implement monetary policy and manage liquidity. Public holdings, in contrast, represent Treasury securities owned by individual investors, financial institutions, and foreign governments, reflecting market demand and investor confidence. Differences between SOMA and public holdings influence interest rates, liquidity conditions, and the overall yield curve.

Table of Comparison

| Category | SOMA Holdings | Public Holdings |

|---|---|---|

| Definition | System Open Market Account (Federal Reserve's securities portfolio) | Debt and securities owned by private investors and institutions |

| Ownership | Federal Reserve | Private investors, mutual funds, pension funds, foreign governments |

| Purpose | Monetary policy implementation and liquidity management | Funding U.S. Treasury debt obligations |

| Security Types | Primarily Treasury securities and federal agency debt | U.S. Treasury securities, corporate bonds, municipal bonds |

| Impact on Economy | Direct influence on interest rates and money supply | Reflects market demand and investor confidence |

| Liquidity | High liquidity due to Federal Reserve operations | Varies by holder type and security |

Overview of SOMA Holdings and Public Holdings

SOMA (System Open Market Account) holdings represent the Federal Reserve's portfolio of U.S. Treasury securities acquired through open market operations to implement monetary policy and stabilize financial markets. Public holdings of Treasury securities include all other investors such as individuals, institutions, foreign governments, and mutual funds, reflecting market demand and investment trends. Comparing SOMA holdings to public holdings highlights the Fed's significant role in influencing Treasury yields and liquidity by adjusting its balance sheet composition.

Composition Differences: SOMA vs. Public Holdings

The System Open Market Account (SOMA) primarily holds U.S. Treasury securities with longer maturities and larger allocations in Treasury notes, reflecting the Federal Reserve's focus on monetary policy implementation. In contrast, public holdings display a more diversified composition, including significant portions of Treasury bills and bonds held by private investors, foreign governments, and mutual funds. This divergence in maturity structure and investor composition highlights the distinct roles and objectives between SOMA and public Treasury holdings.

Role of the Federal Reserve in SOMA Holdings

The Federal Reserve manages SOMA (System Open Market Account) holdings as part of its monetary policy implementation, primarily by purchasing and holding government securities to influence interest rates and liquidity in the banking system. Unlike public holdings of U.S. Treasury securities, which are owned by private investors, foreign governments, and other entities, SOMA holdings are directly controlled by the Fed to stabilize financial markets and support economic growth. This active role distinguishes the Federal Reserve as a key participant in debt markets, balancing public debt management with monetary policy objectives.

Market Accessibility: SOMA vs. Public Investors

SOMA holdings, managed by the Federal Reserve, consist primarily of U.S. Treasury securities acquired through open market operations to implement monetary policy, limiting direct market accessibility for public investors. Public holdings, on the other hand, represent Treasury securities owned by individuals, institutions, and foreign governments, reflecting active participation in the secondary market with high liquidity and accessibility. The difference in market accessibility impacts price discovery and yields, with public investors facing market-driven pricing while SOMA holdings remain insulated from typical market volatility.

Impact on Treasury Yields: SOMA and Public Demand

SOMA holdings, primarily managed by the Federal Reserve, influence Treasury yields by providing stable demand that helps lower long-term borrowing costs compared to volatile public holdings. Higher SOMA participation reduces market supply pressure, leading to decreased yields as the Fed's purchases signal monetary policy direction and foster investor confidence. Public demand fluctuates with economic conditions and risk appetite, causing yield variability driven by market sentiment and liquidity preferences.

Liquidity Considerations in SOMA and Public Holdings

SOMA holdings, comprising securities held by the Federal Reserve, offer higher liquidity due to their role in open market operations and immediate market accessibility, facilitating monetary policy implementation. Public holdings, consisting of securities owned by private investors and institutions, generally exhibit varying liquidity profiles influenced by market conditions and investor demand. The liquidity considerations in SOMA holdings prioritize rapid convertibility and market stability, whereas public holdings balance liquidity with investment objectives and risk tolerance.

Historical Trends in SOMA and Public Treasury Holdings

Historical trends in SOMA (System Open Market Account) holdings reveal consistent growth as the Federal Reserve expanded its balance sheet through large-scale asset purchases, particularly during and after financial crises. Public Treasury holdings, by contrast, have seen fluctuations driven by changes in foreign demand and investor behavior, with foreign central banks and private investors significantly impacting public debt ownership. Over the past decade, the divergence between SOMA and public holdings underlines the Fed's active role in monetary policy versus market-driven shifts in public debt distribution.

Policy Implications of SOMA vs. Public Holdings

SOMA holdings, managed by the Federal Reserve, represent central bank assets primarily aimed at implementing monetary policy through open market operations, contrasting with public holdings, which consist of treasury securities owned by private investors and institutions. The policy implications of maintaining substantial SOMA holdings include enhanced control over interest rates and liquidity, enabling the Fed to influence economic activity and stabilize financial markets effectively. In contrast, public holdings reflect market-driven demand for sovereign debt, impacting fiscal financing costs and signaling investor confidence, but offer limited direct control for monetary authorities.

SOMA Holdings and Quantitative Easing Effects

SOMA holdings represent the Federal Reserve's portfolio of Treasury securities acquired primarily through quantitative easing (QE) programs to support economic stability and liquidity. These holdings influence longer-term interest rates and asset prices by reducing the supply of Treasuries in public hands, thereby lowering borrowing costs. The expansion of SOMA holdings during QE episodes leads to a decline in public holdings, shifting market dynamics and reinforcing monetary policy transmission.

Future Outlook for SOMA and Public Treasury Holdings

SOMA holdings, managed by the Federal Reserve, are expected to evolve with shifts in monetary policy and balance sheet normalization, potentially leading to a gradual reduction in U.S. Treasury securities held. Public Treasury holdings, consisting of debt owned by private investors, institutional investors, and foreign governments, are projected to increase as government borrowing needs grow to finance fiscal deficits. The interplay between SOMA's adjustments and expanding public holdings will significantly influence Treasury yields, liquidity, and overall market dynamics moving forward.

Important Terms

Primary Dealers

Primary Dealers play a crucial role in managing System Open Market Account (SOMA) holdings, acting as intermediaries in the Federal Reserve's open market operations to stabilize liquidity and influence short-term interest rates. SOMA holdings primarily consist of U.S. Treasury securities and mortgage-backed securities purchased by the Federal Reserve, while Public holdings refer to the amounts of these securities held by investors outside the Federal Reserve System, including Primary Dealers, banks, and the general public.

Reserve Balances

Reserve balances fluctuate based on SOMA holdings, which represent the Federal Reserve's assets, while public holdings reflect the market participation of private investors; changes in SOMA holdings directly influence the liquidity available in the banking system through reserve balances. Higher SOMA holdings typically increase reserve balances, enhancing the Federal Reserve's ability to implement monetary policy by managing the supply of reserves in circulation.

Asset Purchase Program

The Asset Purchase Program significantly increased SOMA holdings by acquiring government securities from public holdings to stabilize financial markets and influence interest rates.

Federal Reserve Portfolio

The Federal Reserve's portfolio primarily consists of SOMA (System Open Market Account) holdings, including U.S. Treasury securities and mortgage-backed securities, which represent the central bank's assets acquired through open market operations. These SOMA holdings differ from public holdings, which are the securities owned by private investors, foreign governments, and other non-Federal Reserve entities in the public debt market.

U.S. Treasuries Distribution

U.S. Treasuries distribution shows SOMA holdings account for approximately 20% of the market while public holdings represent around 80%, reflecting Federal Reserve's balance sheet composition versus private investor ownership.

Marketable Securities

Marketable securities in SOMA holdings primarily consist of U.S. Treasury and federal agency securities held by the Federal Reserve, while public holdings encompass similar securities owned by private investors, institutions, and foreign governments.

Nonmarketable Debt

Nonmarketable debt held in SOMA primarily consists of Treasury securities used for monetary policy operations, contrasting with public holdings which represent marketable debt available for public trading.

Indirect Bidder

Indirect bidders in the SOMA Holdings vs Public Holdings case typically acquire shares through third-party intermediaries, enabling them to influence the ownership structure without direct public disclosure. This mechanism often impacts voting rights and control, complicating the transparency of shareholding patterns in corporate governance disputes.

Maturity Structure

Maturity structure analysis reveals that SOMA holdings predominantly consist of longer-term Treasury securities, enhancing interest rate risk management, while public holdings favor shorter maturities, offering greater liquidity and responsiveness to market fluctuations. The Federal Reserve's SOMA portfolio thereby stabilizes monetary policy through strategic duration positioning, contrasting with the public sector's shorter debt instruments aligning with fiscal flexibility needs.

Auction Allotments

Auction allotments in SOMA holdings versus public holdings reveal distinct ownership patterns, with SOMA allocations often concentrated through institutional investors optimizing liquidity and market stability. Public holdings typically display a broader distribution among retail investors, enhancing market participation but potentially increasing volatility due to varied trading behaviors.

SOMA holdings vs Public holdings Infographic